Farewell to the Labuk

By Editor on Saturday, October 2nd, 2021 in Issue 3 - 2021, Publication No Comments

By Editor on Saturday, October 2nd, 2021 in Issue 3 - 2021, Publication No Comments

The Libuk Durian massacre was certainly the bloodiest event in the early history of Tungud. However the saddest incident, which took place the following year, must surely be the story of Suppiah and Leena.

Read more »By gofb-adm on Wednesday, September 29th, 2021 in Issue 3 - 2021, Markets No Comments

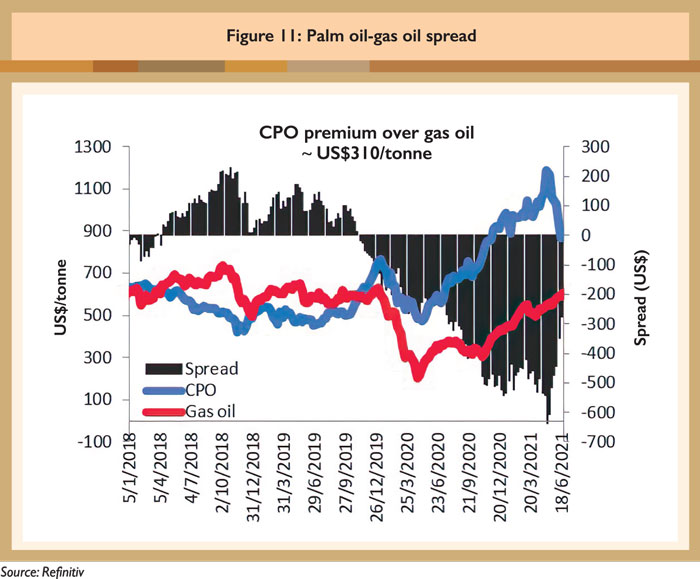

Palm oil prices experienced a rally during the first half (H1) of the year, with the average monthly Malaysian delivered CPO price ranging between a high of RM4,572/tonne in May and a low of RM3,749/tonne in January. The Bursa Malaysia Derivatives Exchange’s CPO Futures (FCPO, Figure 1) third-month benchmark price also experienced a rally during this period, fluctuating between RM3,160 and RM4,525/tonne, trending lower after hitting a record high of RM4,525/tonne on May 12.

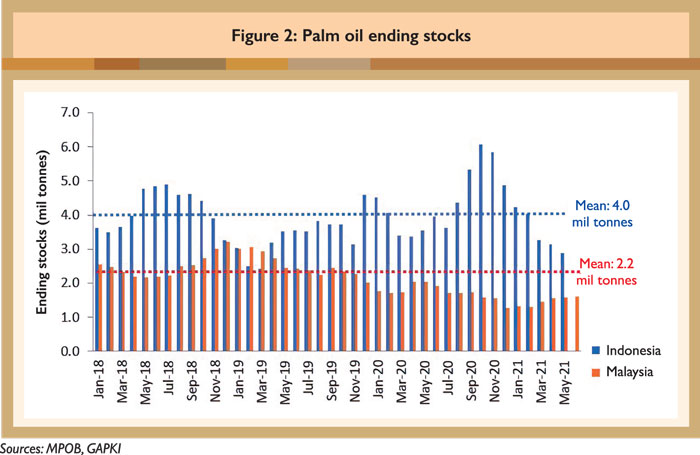

Low palm oil ending stocks in Indonesia and Malaysia kept prices firm. Indonesian Palm Oil Association data showed that Indonesia’s inventories were at 2.9 million tonnes for May, down 18% year-on-year. According to the Malaysian Palm Oil Board (MPOB), inventories in Malaysia were at 1.6 million tonnes for June, down 15% year-on-year (Figure 2). Supply disruptions and rebounding demand led by recovering economic activities from the second half (H2) of 2020 have kept inventories at below-average levels.

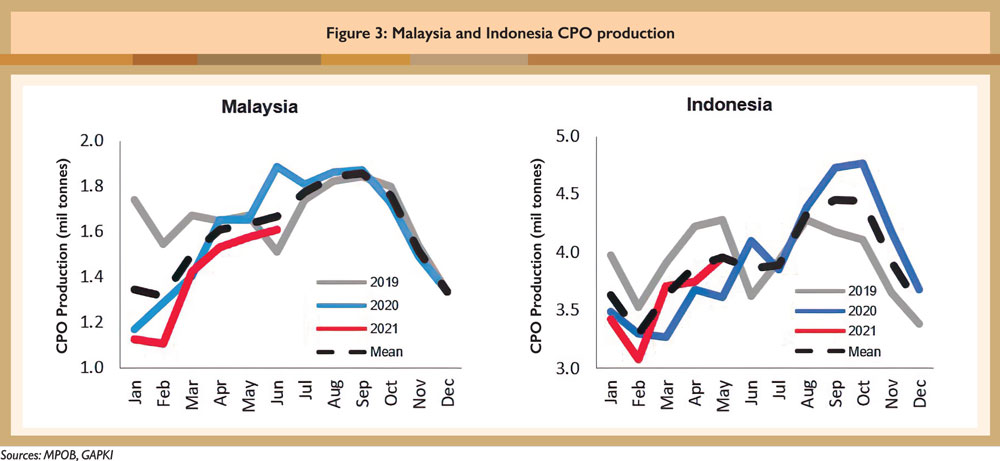

There has been a halt in palm oil output growth over the last three years (Figure 3), mainly due to wet weather conditions, remaining effects of prolonged drought in Q3 2019, lower fertiliser applications over the past few years and labour shortages (primarily in Malaysia). MPOB data showed that CPO production in Malaysia in H1 of 2021 totalled 8.4 million tonnes, down 7.6% compared to the same period in 2020. In contrast, Indonesian CPO production during the first five months of 2021 totalled 17.9 million tonnes, edging up by 3.2% year-on-year, indicating a faster production recovery.

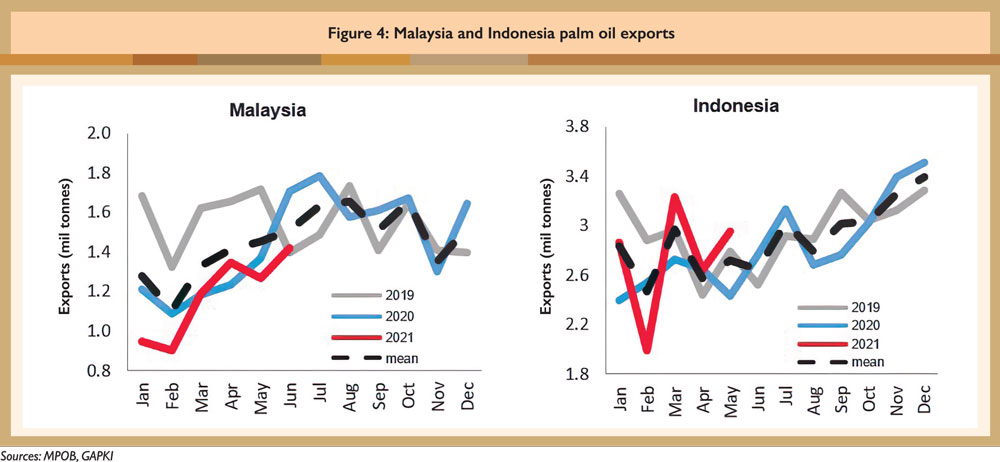

Year-to-date Malaysian palm oil exports were relatively subdued (Figure 4), totalling 7.1 million tonnes for H1, down 9.3% year-on-year. In contrast, Indonesian palm oil exports over the first five months of the year totalled 13.7 million tonnes, up 7.4% year-on-year.

Second half of the year

Production outlook

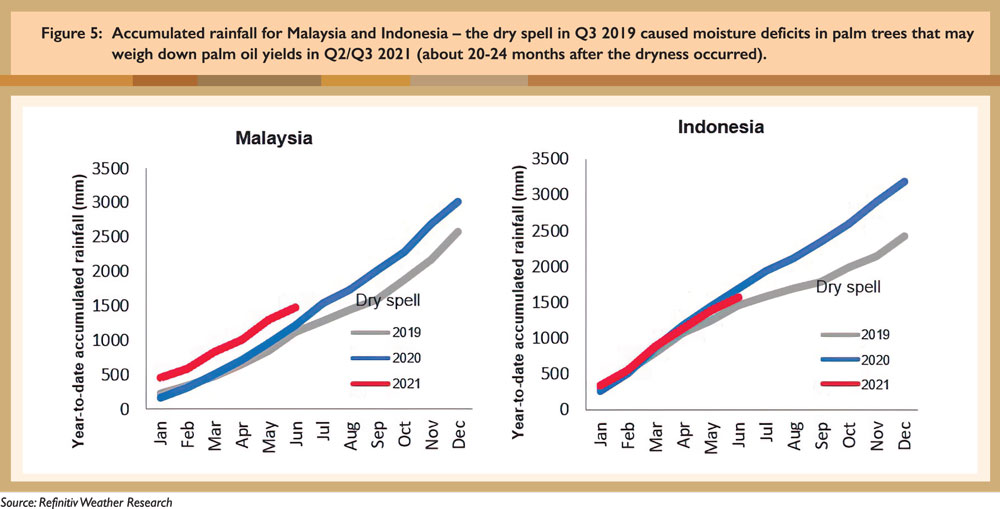

Indonesian CPO production for the whole of 2021 is projected to be higher by 1-3 million tonnes versus 2020 at 47-50 million tonnes. Malaysia’s production is expected to be around 18.7-19.3 million tonnes. The lagged impact of prolonged drought in Q3 2019 (Figure 5) and lower fertiliser applications over past years have capped the upside, but palm oil production in both countries will see seasonal recovery in H2 this year.

Indonesia is poised to have a more robust output recovery relative to Malaysia due to good estate management and no halt in operations or labour shortage. The Malaysian palm oil industry was short of approximately 31,000 harvesters, prompting significant crop losses. Progress in recruiting locals and bringing back foreign workers has been slow in the face of the Covid-19 situation.

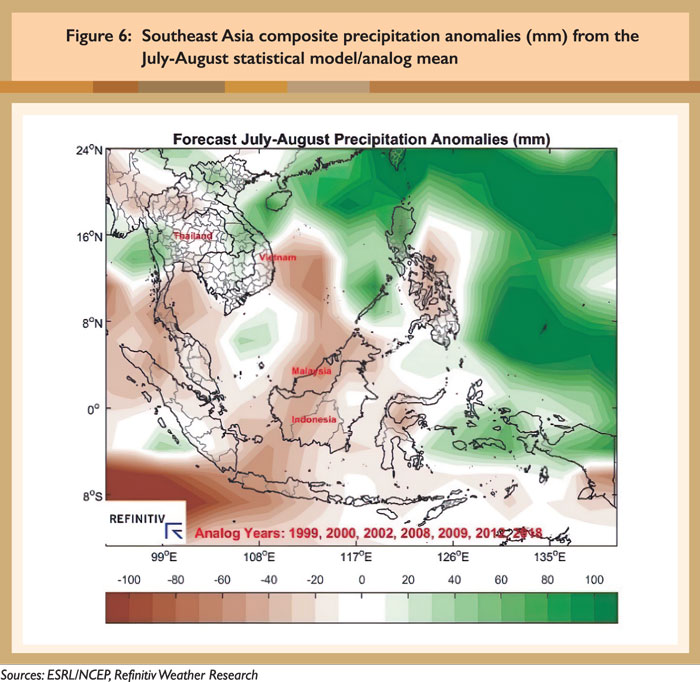

In terms of the weather outlook, the El Niño 3.4 region has trended warmer from a La Niña state towards a neutral negative ENSO state in recent weeks, which would bring drier-than-normal weather conditions across most palm-growing areas in Malaysia and Indonesia in July and August (Figure 6) if the trend continues. Lack of heavy rain will benefit harvest activities, boosting output during this period. September-November could feature wetter-than-normal conditions, which will largely favour oil palm growth in the region.

Demand outlook

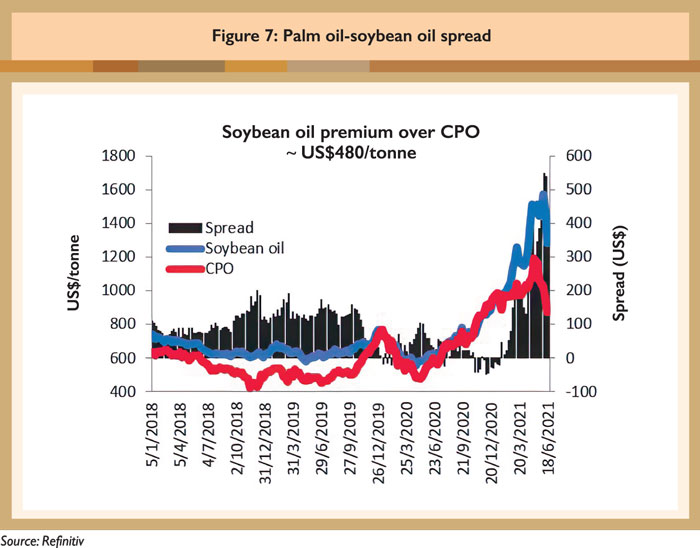

The demand outlook for H2 is pointing more towards upside, with the reopening of the hotels, restaurants and café sector amidst large-scale Covid-19 vaccination rollouts worldwide; this will boost demand in the food and non-food (e.g. oleochemicals and biofuels) industries. Demand is also underpinned by palm oil’s steep discounts to soybean oil, which widened to US$480/tonne by the end of June (Figure 7), making palm oil more attractive versus rival edible oils. The price correction in June has also attracted bargain buying.

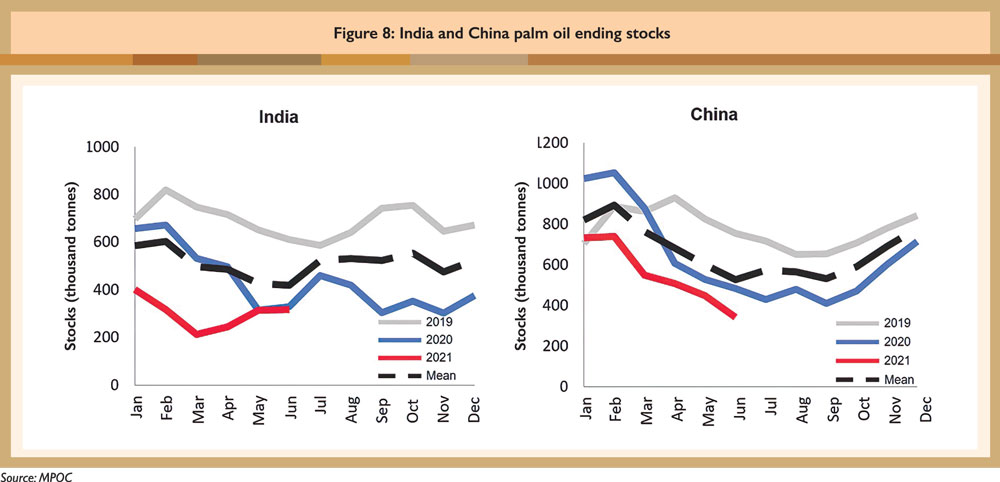

Palm oil inventories in India and China, the two largest consuming countries, remain low (Figure 8), encouraging replenishing activities. Stocks in China for June were estimated at 0.34 million tonnes, down 29% year-on-year, while inventories in India were at 0.32 million tonnes, down 4% year-on-year. Also, warmer weather in summer is conducive to blending, potentially boosting domestic consumption, further depleting inventories and encouraging demand.

Both key producing and consuming countries have revamped tariff structures in favour of boosting demand in H2.

Indonesia adjusted export levies for July, lowering the ceiling rate for CPO to US$175/tonne from US$255/tonne. The export levy starts when CPO prices hit US$750/tonne, with a US$20 increase for every US$50 rise in CPO. Palm oil export duties were also slashed to US$116/tonne for July, versus US$183/tonne in June, in response to falling CPO reference prices. The new palm oil levy is likely to lift exporters’ profit margin and prompt selling abroad.

Supported by the levies, the implementation of the B30 mandate in Indonesia remains an underpinning to sustain considerable domestic consumption since demand for the fuel has been evenly spread in 2021, according to a recent report by Indonesia’s state-owned oil company. The revision of export levies bears no impact on financial backing for the ongoing national replanting programmes targeting 180,000 ha in H2.

India, the world’s largest importer, lowered CPO import tariffs to 10% from 15% for three months, effective June 30, making the effective rate, including other tariffs, 30.25% versus the previous rate of 35.75%. Moreover, India removed RBD palm oil and RBD palm olein from the list of restricted items for a period of six months until Dec 31, prompting palm oil imports to become more appealing compared to rival edible oils. Buyers could take this opportunity to ramp up palm oil imports to meet high festive demand.

However, there are several downside risks for demand. Palm oil imports by key destinations, such as India, slumped earlier this year due to a resurgence of Covid-19 cases in the country. The continued impact of the pandemic will influence global consumption in the food and non-food sectors, and determine the pace of demand recovery in H2.

Also, bumper oilseed supplies in the months ahead and the EU’s policies will negatively impact the market. The revised Renewable Energy Directive (RED II) is poised to cap palm oil as a feedstock for biodiesel in the mid-to-long run. The Belgian government has notified the EU of a draft national decree that is poised to exclude palm-based biodiesel from its market from 2022. Moreover, the EU’s new food safety standards on 3-monochloropropane diol (3-MCPD) and glycidyl fatty acid esters (GE), contaminants found in refined palm oil products, are also expected to weigh on imports.

Price outlook

Palm oil prices have experienced a prolonged rally since last year, fueled by tight supplies and demand recovery. However, the rally tapered off in June (Figure 9). Worries about lacklustre demand and production recovery going forward have depressed palm oil prices recently. Erosions in external vegetable oil markets, such as the Chicago Board of Trade and the Chinese Dalian Commodity Exchange, have also weighed on sentiment.

As Malaysia and Indonesia have entered the peak palm oil production season, prices could be pressured by rising inventories. We believe that palm oil prices will stay elevated, supported by low inventory levels at both origins and destinations, but will remain volatile throughout H2, affected by other market drivers.

Bigger global oilseed production is on the way

Palm oil production is picking up and prices could face pressure if production increases significantly in the coming months. As Indonesia has a faster pace of recovery, H2 production will be dependent to a large extent on the weather factor and stability of estate management in supply performance. The current favourable levy structure is also expected to provide space for companies to increase production capacity, which will lend support to the enhancement of the downstream industry, R&D, scholarship and replanting programmes.

The pace of production recovery in Malaysia will depend on how soon the industry can get an adequate supply of foreign workers; as well as on yield recovery from 2019’s dryness and lower fertiliser applications from previous years.

The US Department of Agriculture (USDA) also indicates more oilseed supplies going forward, with the global soybean production for 2021/22 higher by 21.7 million tonnes from 2020/21 levels to 385 million tonnes. The USDA raised global soybean ending stock estimates for 2021/22 by 3 million tonnes from 2020/21 levels to 94.5 million tonnes, on the back of higher beginning stocks for the US and Brazil. Refinitiv Agriculture Research pegged global soybean production and ending stocks for 2021/22 at 385 million tonnes and 90 million tonnes respectively (estimates as at June).

The USDA raised global rapeseed production by 5.1 million tonnes to 74.1 million tonnes for 2021/22. Global sunflower seed production was raised by 7.3 million tonnes to 57 million tonnes in the coming season. A bumper sunflower crop from the Black Sea region will be entering the market to compete for a share in the months ahead.

Uncertainties in external policies

The US government policy on biofuels remains uncertain. Soybean oil prices tumbled after the news that the US government is considering providing oil refiners relief from the biofuel blending mandate, following a Supreme Court ruling to exempt small oil refiners from biofuel blending requirements. This will limit biofuel production, reducing demand for soybean oil. Talk that the Environmental Protection Agency is re-examining biofuel blending requirements adds to the uncertainty, with any unfavourable adjustments to biodiesel waivers likely to trigger another sell-off.

In addition, China’s plans to strengthen commodity price controls domestically, reflected by its move to auction imported corn and soybean oil to cool domestic prices, is also viewed as bearish for the market.

Supporting drivers

After a prolonged rally since last year, palm oil prices have been starting to moderate but will stay elevated. The historical peak of RM4,525/tonne in the five weeks from May 12 to June 18 – despite the recent bearish benchmark of FCPO of RM3,262/tonne – should keep the market optimistic. Year-to date average prices are de facto higher than an expected average of RM2,600-2,650/tonne.

The industry holds mixed views on the CPO price trend, with the Malaysian Palm Oil Council forecasting prices to range between RM3,500 and RM3,800/tonne in the coming three months, supported by rising export prospects while output is expected to increase marginally. Reuters technical analysis suggests that FCPO in Q3 may bounce to RM3,746-3,844/tonne, before dropping towards RM2,927-3,232/tonne levels. Some industry players also expect palm oil prices to soften further in H2 after registering an all-time high CPO price in May.

Price volatility will stay in H2. However, increased enabling environments in producer countries and encouraging demand especially from China and India, compounded by several supporting drivers in the near/mid-term should spark positive sentiment. Rising gas oil prices are supportive of the palm-based biodiesel market as Indonesia is progressing towards its output target of 9.2 million kilolitres, a target set for the B30 mandate this year.

Improved global demand will persist amidst mass vaccination rollouts, on the back of a steep discount to rival vegetable oils, low inventories in key consuming countries and favourable tariff structures. The US will be a factor to consider due to unfavourable weather, and biofuels policy that may lower the demand and output growth of soybean oil. This will give palm oil a likely advantage in H2.

Tan Kian Pang

Senior Analyst, Agriculture Research

&

Lim Suet Yiing

Senior Analyst, Oil Research,

Refinitiv

This is a slightly edited version of the report prepared by Refinitiv with feedback from the CPOPC Secretariat. The full version is available at: https://www.cpopc.org/wp-content/uploads/2021/07/2021_PALM-OIL-SUPPLY-AND-DEMAND-OUTLOOK-REPORT-WITH-REFINITIV-1.pdf

By gofb-adm on Wednesday, September 29th, 2021 in Issue 3 - 2021, Markets No Comments

In the context of trade negotiations to update the EU-Chile Association Agreement, the European Commission (EC) submitted a text proposal in June for a chapter on ‘Sustainable Food Systems’. This is part of the EU’s initiatives to support a ‘green transition’, and promote responsible and sustainable value chains.

The chapter aims at ‘strengthening policies and defining programmes that contribute to the development of sustainable, inclusive, healthy and resilient food systems’. It also emphasises ‘cooperation between the Parties to improve sustainability of the respective food systems’.

The proposed chapter is clearly an issue that requires greater attention, as it could be of great relevance to Malaysia for trade in sustainable palm oil.

Earlier this year, the EC published its updated approach to trade negotiations in its ‘Trade Policy Review – An Open, Sustainable and Assertive Trade Policy’, which sets out the EU’s trade policy agenda for the coming years.

With respect to trade agreements, the strategy underlines the EU’s commitment to reinforcing its engagement with various trading partners; concluding ongoing trade negotiations; and creating the necessary conditions for the ratification of concluded trade agreements. Notably, the strategy states that the EU intends to include a chapter on sustainable food systems in future trade agreements.

The proposed chapter does not introduce binding commitments, but focuses on cooperation and collaboration between the Parties. The purpose is to strengthen policies at the bilateral and international levels in favour of ‘sustainable, inclusive, healthy and resilient food systems’.

The proposed chapter focuses on cooperation with respect to:

The proposal defines ‘sustainable food systems’ as ‘a food system that delivers food security, safety and nutrition for all in such a way that the economic, social and environmental bases to generate food security and nutrition for future generations are not compromised’.

The essential characteristics of sustainable food systems are described as:

With respect to the sustainability of food production, processing, marketing and consumption, the proposal provides that the Parties would, inter alia, commit to cooperation to reduce the use of antimicrobials, chemical pesticides and fertilisers, as well as to promote more sustainable food production, such as organic farming.

Additionally, the Parties would commit to cooperation to reduce the environmental and climate impact of food production; support sustainable food production so as to contribute to reducing greenhouse gas emissions; and ‘increase carbon sinks and reverse biodiversity loss’. Moreover, the Parties would commit to collaboration to promote ‘the uptake of healthy and sustainable diets, reducing the carbon footprint of consumption’.

In the fight against agri-food fraud and antimicrobial resistance, the Parties would commit to cooperation to establish an action plan with the aim of pursuing the objectives agreed within the chapter; to establish a Subcommittee on Sustainable Food Systems under the Sanitary and Phytosanitary Subcommittee; and to cooperate within relevant multilateral fora.

Cooperation at the multilateral level is aimed at fostering ‘the global transition towards sustainable food systems that contribute to the achievement of internationally agreed environmental, nature and climate protection objectives’.

Relevance to sustainable palm oil

The various characteristics of sustainable food systems do not only address the ‘sustainability of food production’, but also the sustainability of food processing and marketing, as well as the sustainability of food consumption including healthy diets.

These characteristics will have direct relevance to Malaysia. For example, the country has made significant efforts to ensure the sustainability of its palm oil industry.

On Jan 1, 2020, the government made it mandatory for oil palm growers and palm oil producers to be certified under the Malaysian Sustainable Palm Oil (MSPO) standard. This standard ensures responsible and sustainable production by oil palm smallholdings, plantations and palm oil processing facilities, as well as transparency and traceability along the value chain.

As at Dec 31, 2020, nearly 90% of oil palm cultivation had obtained the certification. Additionally, 428 of the country’s 452 palm oil mills – about 95% of the facilities – had received certification.

These actions are real, measurable and adopted to protect what is not only a precious resource for humanity, but Malaysia’s most important asset and comparative advantage: its forests and unique ecosystem.

The proposed chapter on sustainable food systems could therefore provide an opportunity to ensure that Malaysia’s efforts towards sustainable palm oil production are considered and recognised by the EU in future trade negotiations.

MPOC Brussels

By gofb-adm on Wednesday, September 29th, 2021 in Issue 3 - 2021, Markets No Comments

Trade policy within the European Union (EU) has undergone significant changes in recent years. On the basis of the 2015 ‘Trade for all – Towards a more responsible trade and investment policy’ strategy, the European Commission (EC) has placed greater emphasis on labour rights and environmental matters. These issues have become important factors in the context of the EU’s trade policy and agreements.

In a February 2021 review, the EC published an updated approach toward ‘an open, sustainable and assertive trade policy’ agenda. With respect to trade agreements, it underlines the EU’s commitment to:

The EU also intends to include a chapter on sustainable food systems in future trade agreements. A draft proposal was recently submitted for discussion in the context of the EU-Chile trade negotiations.

Sustainability has become a political issue, as reflected in recent trade agreements. On Dec 16, 2018, Indonesia and the countries within the European Free Trade Agreement (EFTA) – namely, Iceland, Liechtenstein, Norway and Switzerland – concluded the Indonesia-EFTA Comprehensive Economic Partnership Agreement (CEPA).

The CEPA enters into force on the first day of the third month after two EFTA States and Indonesia deposit their instrument for ratification. It is expected to take place this year.

When the CEPA takes effect, Switzerland, for example, will provide specific concessions for certain palm oil products. These comprise tariff-rate quotas for crude palm oil, palm stearin and palm kernel oil. Initially, the tariff-rate quota will stand at 10,000 tonnes; this will gradually increase over five years to 12,500 tonnes.

Indonesia will have to reciprocate by meeting requirements of sustainability and traceability. Its palm oil exports to Switzerland will have to comply with Article 8.10 on ‘Sustainable management of the vegetable oils sector and associated trade’, which is included in the CEPA chapter on Trade and Sustainable Development.

In April 2021, Switzerland further adopted an Ordinance on Preferential Importation of Sustainable Produced Palm Oil from Indonesia, in order to implement Article 8.10. The Ordinance will enter into force at the same time as the CEPA.

Article 2 of the Ordinance lists the four certification systems that will be valid as proof of compliance with the sustainability objectives, namely:

Notably, the Ordinance does not include the Indonesian Sustainable Palm Oil certification.

The EU’s Most Favoured Nation rate currently provides for a relatively low tariff for palm oil products. Its recent free trade agreements (FTAs) have gone further to provide important concessions to palm oil-producing third countries or countries trading in palm oil-derived products with the EU.

For example, the EU has totally liberalised trade in palm oil and derived products, and fully eliminated tariffs on all relevant tariff lines under:

Another example is the EU-Mercosur Association Agreement, which has been concluded and is pending ratification. Under this, the EU will provide a significant reduction of tariffs for certain palm oil products, notably duty-free market access for crude palm oil (but not for technical or industrial uses); and a reduction from 12.8% to 7% for solid palm oil fractions, whether or not refined. While the majority of the Mercosur countries do not produce palm oil, Brazil is the world’s eighth-largest producer.

Trade links with Southeast Asia

Over the past several months, the EU has recalled its commitment to strengthen engagement with the Association of Southeast Asian Nations (ASEAN). However, a prospective EU-ASEAN trade agreement remains a longer-term agenda. If it materialises, it should address trade in vegetable oils, including palm oil, at the region-to-region level.

In the meantime, two bilateral trade agreements have been concluded. Under the FTA with Singapore and Vietnam respectively, the EU has not fully liberalised trade in palm oil and derived products, but has significantly reduced tariffs. It must also be noted that the EU-Vietnam FTA does not liberalise tariffs on a multitude of headings relevant to palm oil, such as palm kernel oil.

As Indonesia looks ahead to the CEPA, Thailand and the Philippines have expressed their willingness to resume negotiations with the EU. Negotiations between the EU and Malaysia were launched in 2010, but were suspended in 2012.

Malaysia stands to significantly benefit from a preferential trade agreement with the EU. The discussions would provide an opportunity to negotiate tariff reductions or other forms of preferential market access – through facilitated and mutually-recognised certification schemes – for palm oil products.

Malaysia has already demonstrated its commitment to producing sustainable palm oil. It is therefore essential that the future EU-Malaysia trade agreement eliminates tariffs on ‘green goods’ like sustainable palm oil. The pact should further ensure that any related sustainability criteria or certification schemes are mutually recognised, and that there is no discrimination against the Malaysian Palm Oil industry.

The eventual EU-Malaysia trade agreement should also address the non-tariff measures adopted by EU member-states, and the anti-competitive practices often implemented in that market by private operators. These include the use of ‘no palm oil’ or ‘palm oil-free’ labels.

Once an agreement is in place, it should introduce regular bilateral dialogues and transparency requirements, so that any issue affecting trade in palm oil and derived products can be raised and resolved bilaterally. Such issues could be dealt with at the technical, legal and diplomatic levels, and linked to the broader economic context of reciprocal concessions and trade advantages.

The UK moves on

Given Britain’s withdrawal from the EU from March 29, 2019, it will not be part of an eventual EU-ASEAN trade agreement. However, the UK has expressed strong interest in direct engagement with ASEAN.

Brexit has had a wide-ranging impact on the UK’s trade and investment relations with third countries. In order to maintain preferential trade, the UK has negotiated ‘roll over’ trade agreements, to allow for the continued application of terms offered under existing EU trade agreements with certain third countries.

At the same time, the UK has been exploring new ways to collaborate with ASEAN member-states. In August 2020, the first formal engagement was held through the UK-ASEAN Economic Dialogue. The parties committed to strengthening trade ties; mitigating the economic impact of the Covid-19 pandemic; and pursuing sustainable growth.

Preparatory work to negotiate a preferential trade agreement between the UK and Malaysia was initiated at the first meeting of the UK-Malaysia Joint Committee on Bilateral Trade and Investment Cooperation, held in November 2020.

It endorsed key areas of cooperation, including education; standardisation and conformity assessment; and development of micro-, small- and medium-enterprises.

The Joint Committee will also provide a platform for Malaysia to address discriminatory trade practices that affect palm oil, such as negative claims by certain food businesses and retailers in the UK.

MPOC Brussels

By gofb-adm on Wednesday, September 29th, 2021 in Issue 3 - 2021, Markets No Comments

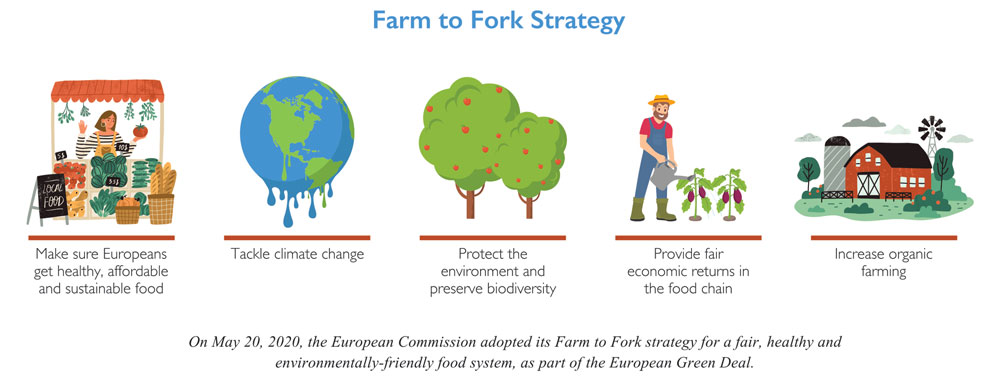

The European Commission (EC) published its Farm to Fork (F2F) strategy in 2020, as part of the European Green Deal initiative. The strategy aims at making ‘the entire food chain from production to consumption more sustainable and neutral in its impact on the environment’.

An initiative under the strategy this year is the EU Code of Conduct (the Code) for responsible business and marketing practices in the food supply chain, linked to a monitoring framework.

The Code is intended to enhance sustainable practices at all stages of the food chain in order to ultimately increase the sustainability of the food system, and reduce the overall environmental footprint of the food industry and the retail sector.

On July 5, 2021, the EC, together with industry stakeholders, officially launched the ‘EU Code of Conduct on Responsible Food Business and Marketing Practices – A common aspirational path towards sustainable food systems’. The same day, 65 signatories become the first companies and associations to embrace it.

They comprise 26 food manufacturers (including Barilla, Ferrero, Mondelez, Nestlé and PepsiCo); 14 food retailers (including Ahold Delhaize and Carrefour); one from the food service sector; and 24 associations (including the European association of trade in cereals, oilseeds, pulses, olive oil, oils and fats, animal feed and agrosupply; the European farmers and agri-cooperatives; and the EU vegetable oil and protein meal industry association).

The Code is not only open to companies and associations in the food sector, but also to any organisation with an interest in sustainability. It has been reported that financial institutions, for example, may sign up with a view to implementing it in their operations; or non-governmental organisations (NGOs) could apply it in partnership with food businesses, to promote their sustainability.

Importantly, this is an industry code that has been developed by EU associations and companies, with active involvement and input from other stakeholders – including international organisations, NGOs, trade unions and trade associations – and together with the EC services.

The EC played the part of the organiser, being closely involved in the preparation of the Code and in the organisation of meetings. It will also oversee implementation.

The EC intends to present the Code at the UN Food Systems Summit later this year. This appears to be the reason why the drafting of the Code took only three months from Jan 26, 2021. Members of the European Parliament and of the EC worked with high-level stakeholders on the drafting process.

On the occasion of the launch, Stella Kyriakides, European Commissioner for Health and Food Safety, stated: “Today we are marking one of the first deliverables in our work under the [F2F] strategy towards a healthy and environmentally-friendly food system. Close cooperation between all actors is essential to achieve a successful transition to sustainable food systems.

“The EU Code of Conduct will facilitate this cooperation, building on the commitments the food industry has already made and encouraging more ambitious action. The European food industry is already known for the quality and safety of its products. It should now also become the golden standard for sustainability.”

The F2F strategy sets out a long-term vision to transform the way in which food is produced, distributed and consumed. The Code covers all major aspects of sustainability in food production and reflects the goals and ambitions of the strategy and of the European Green Deal.

Commitments of the signatories

The Code sets out indicative actions that actors in the food supply chain – for instance food processors – are voluntarily able to take on in order to improve their sustainability.

Associations and companies that sign the Code commit to accelerating their contributions to the transition towards sustainable food systems. With their pledges, the signatories endorse the objectives set out in the Code and encourage similar companies to participate.

The main targets for signatories are the so-called ‘middle actors’, such as food manufacturers, retailers and food service operators. The Code provides a framework to support these companies in achieving the ambitious commitments required. In addition, having associations on board is viewed as an important element for the rest of the industry, showing the way to their members.

The Code provides for two levels of commitments:

Companies are to report on their progress by submitting a summary with relevant extracts of their latest available Environmental, Social and Governance reports or Non-Financial or Corporate Sustainability reports, and/or any other relevant information that would allow the evaluation of the progress made by companies with respect to their commitments under the Code.

For EU associations, there is a set of objectives, each with its targets and indicative actions that promote a shift towards healthy and sustainable consumption patterns. The objective is to improve the impact of food processing, retail and food service operations on sustainability, and to improve the sustainability of the food value chains in relation to primary producers and other actors in the chain. Associations are to report on their progress on a yearly basis.

Seven aspirations

Signatories to the Code are assumed to share its seven aspirational objectives, together with the potential actions suggested:

The EC considers it ‘essential to complement legislative proposals with voluntary, non-regulatory initiatives addressed to pioneers in the industry that are keen to support the green transition’. As set out in the F2F strategy, the EC will monitor the commitments under the Code and consider legislative measures if progress is insufficient.

Large companies will have to submit an annual report on their progress before the end of April each year. Small- or medium-size enterprises that are not able to report annually will be allowed to provide simplified reports every two to three years.

The Code suggests that companies, if able, should apply risk-based due diligence processes to identify, map and prioritise measures to address adverse environmental, social and economic impacts. Various established guidelines, principles, standards and frameworks on due diligence and responsible business conduct/corporate social responsibility already exist.

The ‘OECD-FAO Guidance for Responsible Agricultural Supply Chains’ is an internationally recognised example, providing guidance for companies and producer countries on social and environmental risk reduction in agri-food supply chains. A non-exhaustive list of guidelines and initiatives is supposed to be made available on the website for the Code.

Implications for the palm oil sector

The Code’s aspirational objective No. 7 – ‘ Sustainable sourcing in food supply chains’ – appears to be the most relevant matter related to palm oil production and use in the food chain. Two aspirational targets are set out within this objective:

In this context, it is important to emphasise that Malaysia’s sustainable palm oil production does not contribute to deforestation, forest degradation and destruction of natural habitats.

The Code also identifies the indicative action of ‘Transformation commodity supply chains’, which consists of:

On the requirement of scientifically robust sustainability certification schemes for food, it should be underlined that the Malaysian Sustainable Palm Oil (MSPO) standard mandates responsible and sustainable production by oil palm smallholdings and plantations, and palm oil processing facilities. The MSPO also enables transparency and traceability along the value chain.

One of the ‘Guiding Principles’ of the Code is that signatories ‘aim to base their contributions towards the objectives of this Code on robust scientific evidence, where available’. Recognition of the science-based MSPO standard is of paramount importance for Malaysian Palm Oil to become a part of the sustainable food supply chain recognised by initiatives like the Code.

The success of the Code and its objective of becoming the new ‘golden standard for sustainability’ will ultimately depend on the number of signatories at both company and association level, as well as the actual implementation of the commitments.

The way the EC monitors the voluntary commitments will determine whether the Code as a ‘soft’ instrument is sufficient to fulfil the ambitious F2F strategy and Green Deal sustainability objectives, or whether a ‘hard’ legislative instrument will have to be proposed to reach the targets.

Uthaya Kumar

MPOC Brussels

By gofb-adm on Wednesday, September 29th, 2021 in Issue 3 - 2021, Sustainability No Comments

Palm oil production forms the backbone of economic activity in many Indonesian communities today. The sector holds vast potential to alleviate poverty by providing employment and raising income levels, thereby improving living standards.

With increasing scrutiny of human rights and labour issues in the palm oil industry, it is crucial for producers to assume full responsibility for sustainable practices, including improvements to social infrastructure in smallholder communities. There is also a need to measure and validate the progress made.

Musim Mas, one of the largest palm oil corporations globally, has long worked on improving the social needs of smallholders in Indonesia, including those in remote areas. The community development programmes cover education, healthcare services, infrastructure, disaster relief measures and environmental conservation. This has benefited farmers, children and teachers, as well as the environment.

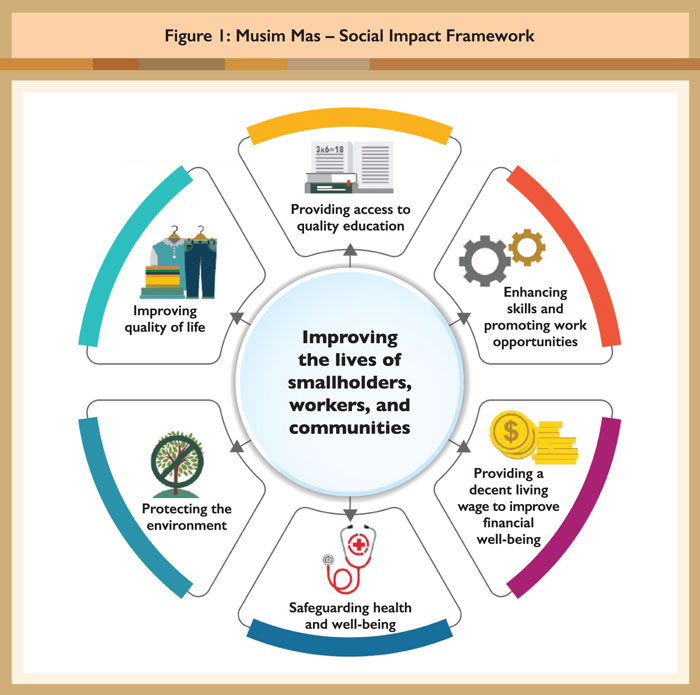

The company has also been collecting vital data to measure the efficacy of its social development programmes, based on its updated Sustainability Policy launched last year. Its inaugural Social Impact Report (SIR), released in May this year, includes a comprehensive Social Impact Framework (Figure 1). The SIR will serve as a guide in reviewing strategies and efficiently focusing resources on programmes that have the biggest impact on improving quality of life.

The success of the programmes is indicated by these main findings of the SIR:

Supporting smallholders

A key aspect of the SIR was to look at the impact of the programmes on smallholders, who play a pivotal role in the company’s supply chain. Smallholders, defined as individuals with farms smaller than 25 ha, are estimated to cultivate around 40% of Indonesia’s oil palm planted area.

Musim Mas works with more than 1 million independent smallholders; its scheme smallholders were also the first to be RSPO-certified in 2010. The company has implemented two programmes for this group – Koperasi Kredit Primer Anggota (KKPA, or Smallholders’ Oil Palm Development Programme) in 1996; and Kebun Kas Desa (KKD, or Village Oil Palm Development Programme) in 2000.

The KKPA is a primary cooperative credit scheme that provides smallholders with practical support, including bank loan guarantees, agricultural training, and the transfer of quality seeds and fertilisers. The scheme targets individual smallholder family units that manage 2 ha of land or less. To get farmers on board, Musim Mas staff went from house to house to explain the benefits of the scheme. They also helped with administrative requirements to obtain land legally, including applications for identity cards.

The KKD, meanwhile, is tailored for holdings under communal ownership and partnership. This outreach initiative promotes economic independence in villages involved in oil palm cultivation; it also aims to improve social conditions in communities in surrounding areas.

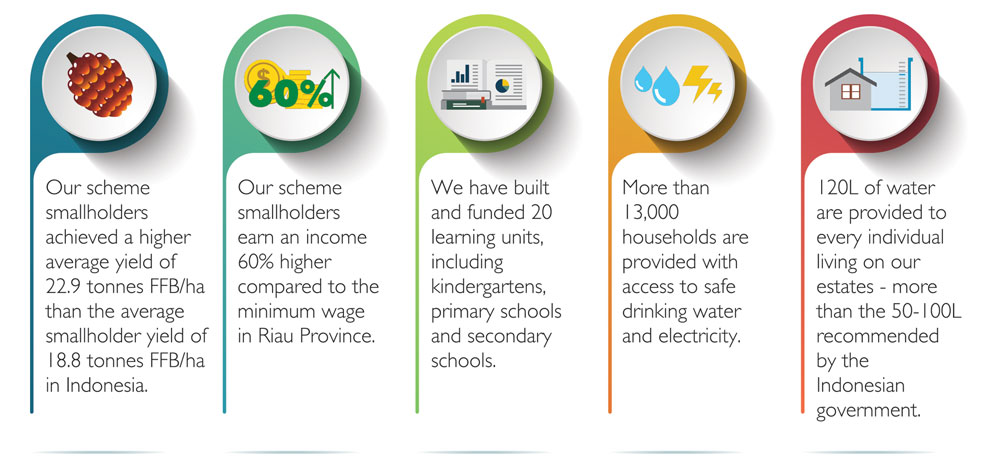

Training is provided to growers – both men and women – as part of the KKPA and KKD programmes. In 2019, Musim Mas conducted 132 training sessions to enhance skills and knowledge. With this, as well as access to higher quality seeds, smallholders have been able to increase the yield of fresh fruit bunches. In 2019, farmers involved in both programmes produced an average of 22.9 tonnes/ha/year – or 22.2% higher than the average RSPO-certified smallholder at 18.8 tonnes/ha/year.

Smallholders under the Musim Mas programmes also enjoy an average wage of 4,343,773 Rupiah (~US$310) per person/month. This is more than 60% higher than the minimum wage in Riau Province of 2,662,026 Rupiah (~US$190). With better income, many farmers have been able to ensure that their children complete higher education.

Rural development measures

Education is fundamental in paving the way to improved livelihoods and social mobility. Since 2002, Musim Mas has been supporting children’s education across Indonesia through the Yayasan Anwar Karim (YAK, or Anwar Karim Foundation); this was set up in memory of the late founder of Musim Mas. The YAK has facilitated his passion for providing quality education to children and youth, among other social welfare activities. In 2019, the operating costs of Anwar Karim schools exceeded 16 million Rupiah.

To date, Musim Mas has built and funded 20 learning units, comprising nine kindergartens, nine primary schools and two secondary schools. Of the 5,983 students enrolled, 47% are girls. In 2013, Musim Mas built the first secondary school at PT Guntung Indamannusa; construction of the second school was completed in 2019 at PT Musim Mas.

Quality teaching jobs are also offered, especially to those from the local community. The schools have received an ‘A’ grade from the Education Ministry. Musim Mas takes pride in providing education for rural children and improving the welfare of teachers, thereby creating a positive learning environment.

Musim Mas is further dedicated to improving infrastructure in remote communities and workers’ compounds. Projects to date include access to utility supplies for more than 13,000 households; construction of roads, mosques and religious centres; provision of free healthcare services at 26 clinics; and upholding of food security.

Fire prevention strategies

Musim Mas takes a serious stance on fire prevention and a deforestation-free supply chain. Forest fires and haze pollution have been a long-standing problem in Indonesia. Musim Mas has therefore rolled out special programmes on sustainable farming policies and fire-free villages. It operates a strict zero-burning policy at all new developments and during replanting, and maintains teams of highly-trained firefighters at each of its plantations. The company’s fire patrol teams and fire monitoring towers enable the early detection of fires.

As part of its Fire-free Village Programme, Musim Mas conducted 148 training sessions at 74 villages covering 458,361 ha in 2019. The topics included alternative land clearing methods and fire prevention, monitoring and suppression. The SIR found that local communities have adopted non-fire farming methods, ever since they began to understand the impact and danger of forest fires. Over the years, there has been an 85% drop in the number of fire incidents within Musim Mas’ concessions – from 89 in 2015 to 16 in 2019.

To combat forest fires beyond its concession areas, the company sees the importance of working with other stakeholders and supporting local communities in adopting alternatives to the slash-and-burn method for land clearing. As a founding member of the Fire-free Alliance – a multi-stakeholder platform set up in 2016 to support the commitment to a haze-free ASEAN by 2020 – Musim Mas has shared information and resources toward a lasting solution.

As a leading sustainable palm oil player, Musim Mas recognises its responsibility and influence in continuing to improve the social and labour conditions of local communities and workers within the industry. The impact can be widened through multi-stakeholder initiatives with government bodies, industry stakeholders and civil society organisations.

Musim Mas

Headquartered in Singapore, Musim Mas is a privately owned, vertically integrated company involved in each point of the palm oil value chain.

By gofb-adm on Wednesday, September 29th, 2021 in Issue 3 - 2021, Nutrition No Comments

In March and April, respectively, retailers Colruyt in Belgium and Lidl in Germany announced the implementation of Eco-Score, a new front-of-pack (FoP) labelling scheme for some of their products. The label aims at indicating the environmental impact of food products in a simplified way.

Eco-Score looks very similar to Nutri-Score, a widely known voluntary FoP nutrition label. Eco-Score was developed in France by the ECO2 Initiative, a consulting firm focusing on environmental transition. The method for calculating the Eco-Score consists of two components:

These elements are converted by the system’s algorithm into a code for a food product consisting of one of five letters of the alphabet, each with a colour – from A (green) for the lowest environmental impact of a product, to E (red) for the highest environmental impact.

On its part, Nutri-Score is a colour-coded system that rates the nutritional value of a food product by assessing the content of key nutrients: salt, fat, saturated fat, sugar and total calorie count. Unlike the ‘traffic light’ label, which highlights key individual nutrients, the Nutri-Score system – introduced in France in 2017 – provides a single score for the entire product, giving consumers an overall assessment of the product.

Based on an algorithm, Nutri-Score gives a rating to any food except single-ingredient foods and water. The rating ranges from dark green A (best) to red E (worst), by weighing the prevalence of ‘good’ and ‘bad’ nutrients.

For both Nutri-Score and Eco-Score, the very idea of a ‘score’ means that they cannot convey any specific information to the consumer on the actual nutritional properties or the specific environmental impact. Notably, these schemes have outpaced ongoing developments at the EU level.

On May 20, 2020, the European Commission (EC) adopted its Farm to Fork (F2F) strategy for a fair, healthy and environmentally-friendly food system, as part of the European Green Deal.

The strategy announced that, in order to promote sustainable food consumption and facilitate the shift to healthy and sustainable diets, the EC would adopt measures to empower consumers to make informed, healthy and sustainable food choices. In particular, the strategy announced that the EC would propose a harmonised mandatory FoP nutrition labelling.

In relation to environmental labels, the F2F strategy announced that the EC would ‘also examine ways to harmonise voluntary green claims and to create a sustainable labelling framework that covers, in synergy with other relevant initiatives, the nutritional, climate, environmental and social aspects of food products’.

Evolving legal framework

The main question related to claims on food products is how they are substantiated. This concerns claims about nutritional, health or environmental properties. Unlike for nutrition and health claims under Regulation (EC) No. 1924/2006 on nutrition and health claims made on foods, there is currently no specific legal framework in the EU on the substantiation of environmental labels or claims.

Competent authorities in the EU member-states can prohibit environmental claims that they find to be misleading towards consumers on the basis of a case-by-case application of existing consumer protection laws.

In particular, the laws are:

The EC is currently preparing a legislative proposal on ‘substantiating green claims’. The related Inception Impact Assessment (i.e. Roadmap) notes that it concerns ‘claims made in relation with the environmental impacts covered by the Environmental Footprint methods’.

According to the Product Environmental Footprint Initiative, these methods measure the environmental performance of a product throughout the value chain, from the extraction of raw materials to the end of life, using a large variety of categories: ‘Some of them are focused on a single issue, e.g. carbon footprint, whereas some encompass multiple environmental themes.’

The Roadmap points out that, ‘in order not to mislead, environmental claims should be presented in a clear, specific, unambiguous and accurate manner’. The initiative aims to ‘make the claims reliable, comparable and verifiable across the EU – reducing greenwashing (companies giving a false impression of their environmental impact)’. This, in turn, ‘should help commercial buyers and investors make more sustainable decisions and increase consumer confidence in green labels and information’.

According to the EC, a proposal for a regulation on green claims was planned for the second quarter of this year. However, it appears that the proposal has been delayed and will only be published during the second semester of this year. A proposal for a directive on consumer empowerment for the green transition that aims at establishing specific rules to combat greenwashing was similarly expected in the second quarter, but will now likely only be published during the second half of this year.

Mandatory scheme?

Alongside the F2F strategy, the EC published a Report to the European Parliament and the Council regarding the use of additional forms of expression and presentation of the nutrition declaration (FoP Report). This included a reference to schemes providing information on the ‘overall nutritional quality of foods’, such as the Nutri-Score scheme, which has been introduced in various EU member-states.

The FoP Report states that, given the political priority of the F2F strategy – namely the potential of FoP schemes enabling consumers to make health-conscious food choices – ‘it seems appropriate to introduce a legislative proposal on a harmonised mandatory FoP nutrition labelling scheme at EU level’.

In the F2F strategy, the EC announced that, by the fourth quarter of 2022, after launching an impact assessment on the different types of FoP schemes, it intends to prepare such legislative proposal on harmonised mandatory FoP nutrition labelling.

No specific scheme has been recommended in the FoP Report. It appears that schemes providing information on the FoP on the overall nutritional quality of foods, such as the Nutri-Score, do not appear to be appropriate for a harmonised mandatory nutrition labelling scheme under the current legal framework of Regulation (EU) No. 1169/2011 of the European Parliament and of the Council of Oct 25, 2011, on the provision of food information to consumers (FIR).

In particular, they arguably fall short of complying with Article 35(1) of the FIR According to this, the mandatory nutrition declaration may be complemented by a voluntary repetition of the energy value and the amount of nutrients in the principal field of vision (also known as the FoP), in order to help consumers see at a glance the essential nutrition information when purchasing foods. Nutri-Score does not provide for such a repetition of the energy value and the amount of nutrients.

Setting of nutrient profiles

The FoP Report also includes a reference to nutrient profiles. According to the World Health Organisation, nutrient profiling is the categorisation of foods according to their nutritional composition using predefined criteria. Nutrient profiles have a variety of applications around the world, for example, for purposes of regulating food marketing to children.

Nutrient profiling is also commonly used in FoP nutrition labelling schemes. Regulation (EC) No. 1924/2006 on nutrition and health claims made on foods requires the EC to adopt nutrient profiles. According to the F2F strategy, the setting of nutrient profiles to restrict the promotion of foods that are high in fat, sugar and/or salt and to stimulate sustainable food processing and reformulation, is foreseen for the fourth quarter of 2022. Nutrient profiles and their categorisation of foods according to their nutritional composition could also become relevant in determining the ‘overall nutritional quality of food’.

There is no doubt that nutrition labels must be based on science. On Dec 14, 2020, in accordance with Article 29(1)(a) of Regulation (EC) No. 178/2002 of the European Parliament and of the Council of Jan 28, 2002 – laying down the general principles and requirements of food law; establishing the European Food Safety Authority (EFSA); and laying down procedures in matters of food safety – the EC requested the EFSA to provide scientific advice for the development of harmonised mandatory FoP nutrition labelling and the setting of nutrient profiles for restricting nutrition and health claims on foods.

In particular, the EFSA was requested to provide scientific advice on the following:

The EFSA has accepted the proposed deadline and expects to deliver its scientific advice by March 31, 2022. In this context, the EFSA will hold a public consultation on its draft scientific opinion.

The food industry now awaits the EC’s proposal for a regulation on the substantiation of green claims and a proposal for a directive on consumer empowerment for the green transition for 2021. The EC also intends to prepare a legislative proposal on harmonised mandatory FoP nutrition labelling by the fourth quarter of 2022. But in the meantime, schemes like Eco-Score and Nutri-Score are spreading around the EU.

Supporters of Nutri-Score and Eco-Score claim to be transparent and to strictly take into consideration scientific criteria – on nutritional aspects for Nutri-Score and on the environmental impact for Eco-Score. However, these schemes are also criticised as being mere marketing tools.

“A system similar to Nutri-Score for environmental aspects would create more confusion and would be equally misleading as it would be intended not to inform consumers but to tell them what to buy,” a spokesperson of the No-Nutriscore Alliance stated.

Notably, an official of the EU has publicly denounced the “ideological fallacy in describing the Nutri-Score as a panacea”.

In light of all this, it is important for the EU to establish a legal framework requiring companies making green claims to substantiate them. The same should apply to nutrition labels, which should inform and educate consumers rather than simply influence their purchasing decisions. Stakeholders in the agri-food sector should carefully observe both initiatives, taking action to ensure that their legitimate interests are voiced and represented within all relevant fora.

FratiniVergano’s Trade Perspectives©

By gofb-adm on Wednesday, September 29th, 2021 in Issue 3 - 2021, Comment No Comments

The Council of Palm Oil Producing Countries (CPOPC) urges the European Union (EU) to revise its approach on vegetable oils in biofuels under the framework of the revised Renewable Energy Directive; as well as the European Commission’s (EC’s) approaching deadline for adopting rules on certifying low indirect land-use change (ILUC)-risk biofuels and updating the list of high ILUC-risk feedstocks.

The CPOPC reiterates its opposition to the criteria laid down in a Delegated Act from March 2019, where palm oil is the only crop yielding a high ILUC-risk and is thus subjected to a freeze and phase-out from the EU’s renewable energy programme.

The use of ILUC as a policy tool has been fraught with methodological problems and biases from the beginning. Therefore, a new approach, which treats all sustainable vegetable oils equally – based on verified production practices and not on the type of commodity – is urgently needed. After all, commodities in themselves are not responsible for deforestation – it is the practices that matter.

Palm oil was singled out as ‘damaging to the environment’ based on a comparison study that used 2008-16 as a gauge for ILUC. This timeline discriminates against countries that were late in development as their growth during that period affected the most Land Use Change (LUC).

The CPOPC argues that a proper timeline to determine the sustainability of vegetable oils for renewable energy should be 1960-2016. This provides an equitable comparison where the dynamic contribution of palm oil to the sustainable development of Indonesia and Malaysia in post-colonial times can be highlighted against global LUC.

This further allows the consideration of new data on LUC which was not available to the EC at the time of its consideration of ILUC. A study by Nature tracked LUC from 1960-2019 and identified 43 million sq km from the Global North to the South. Estimates on palm oil cultivation globally put it at a mere 250,000 sq km.

The global ambition to decarbonise is one of supreme urgency. The recent decision by G7 countries to back off ambitions for electric vehicles is a clear signal that biofuels are a needed tool in fighting climate change without disrupting global economies.

The EU’s bias against palm oil threatens its own ability to decarbonise its transport and energy sectors. Clear evidence of its bias can be seen in its analysis of Annual Net Increase of Harvested Area 2008-16, which highlighted palm oil as the highest at 4%. This puts palm oil at the highest risk of ILUC if one only looks at the percentage.

It must be noted that the same analysis showed considerably larger land footprints of other vegetable oils. Palm oil started at a base point of 15.369 kha, while rapeseed and soybean started at 30.093 kha and 96.380 kha respectively. The EU analysis granted rapeseed an annual net increase of 1%.

This is a clear distortion of facts. Had palm oil producing countries developed at the same pace as rapeseed producing countries, palm oil would have shown a 2% increase instead of 4%. The most apparent distortion of facts is in granting soybean 3% based on a start point and an annual increase of harvested area that is more than four times larger than oil palm.

Seen in this perspective, the CPOPC argues further that the energy yield per hectare of land used for biofuels must be properly included for fair analysis. Scientific research has shown that palm oil has an energy efficiency that is four times that of rapeseed or soybean. Once this knowledge is applied to the EU analysis on land use of vegetable oils, it would place oil palm as the most efficient crop for renewable energy.

In addition to land use, recent studies on the environmental impacts of tilling and heavy agri-chemical use for soybean and rapeseed demand that the EU includes the environmental impacts of these vegetable oils as their contribution to climate change, as this is more quantifiable than the ILUC supposition.

Confidence in producer countries

The major palm oil producing countries of Indonesia and Malaysia, both of which have interests in the EU’s biofuels programme, have shown commitment and concrete actions as to the sustainability of their production.

The Indonesian moratorium on new licenses for oil palm and Malaysia’s commitment to cap the cultivated area are just two examples of sustainable land use management. The significant decrease of wildfires and deforestation in Indonesia provide firm evidence of its commitment towards sustainable vegetable oil production.

CPOPC credits the two countries for this phenomenon, as both strive towards sustainable management of their natural resources, and the positive impact of oil palm in lifting millions of farmers out of poverty.

The implementation of national certification schemes in the Indonesian Sustainable Palm Oil (ISPO) and Malaysian Sustainable Palm Oil (MSPO) has also been instrumental in quantifying the sustainability of production.

The CPOPC acknowledges the EU’s concerns on the efficiency of voluntary certification schemes and looks forward to proving the efficiency of mandatory national schemes in removing deforestation from EU imports.

The ISPO and MSPO are without peer in the global production of vegetable oils. The CPOPC believes that these twin certification schemes provide the right path towards the Sustainable Development Goals (SDGs) for both the EU and palm oil producing countries; ultimately, this can be a global model for sustainable vegetable oils.

Palm oil producing countries look forward to the EU-ASEAN Joint Working Group on sustainable vegetable oils where a holistic and non-discriminatory approach towards vegetable oils can be developed to meet the SDGs.

CPOPC

This is a slightly edited version of an opinion piece posted on June 23, 2021 at: https://www.euractiv.com/section/energy-environment/opinion/cpopc-calls-on-eu-to-adopt-non-discriminatory-biofuels-policy-to-fight-climate-change/

By gofb-adm on Wednesday, September 29th, 2021 in Issue 3 - 2021, Cover Story No Comments

In recent years, EU stakeholders have been considering the introduction of a carbon border adjustment mechanism (CBAM). The idea is that, since the EU is heavily investing in a greener economy – which will raise production costs for its manufacturers – companies could be faced with less ‘green’ but more competitive ‘like products’ from outside the EU, where environmental regulation may be less strict and production less costly. Therefore, the EU is considering a mechanism that would penalise imports of carbon-intensive goods in order to level the playing field.

In the EU, certain emissions are currently regulated through its Emission Trading System (ETS). This is based on the ‘cap-trade system’ principle, where a limit is set on the amount of certain greenhouse gas (GHG) emissions that may be emitted by defined industry sectors. Within the cap, companies can receive or buy allowances that can be traded with other companies.

The cap is then linearly reduced over time so that the total emissions decrease. The ETS covers the electricity and heat generation industry; commercial aviation within the European Economic Area; aluminium production; and certain energy-intensive industrial sectors like cement, glass and oil refineries. It does not apply to the agricultural sector.

A proposal for review of the ETS was published on July 14, 2021, as part of the EU’s ‘Fit for 55’ legislative package. The proposal extends its scope to the maritime sector and foresees the establishment of a separate self-standing ETS from 2025 for road transport, as well as for energy efficiency of buildings.

A main criticism of the ETS concerns the free allocation of allowances, which is used to safeguard ‘the international competitiveness of industrial sectors at risk of carbon leakage’. Carbon leakage refers to the situation in which EU production moves to non-EU countries that have less ambitious emission rules and lower production costs, due to less burdensome climate policies. Industries that receive free allowances are not obliged to reduce emissions at the same pace as industries that do not receive free allowances.

A 2020 report by the European Court of Auditors noted that industries receiving free allowances continue to represent 94% of EU industrial carbon emissions. In order for the EU to reach its target of zero emissions by 2050, free allowances would need to be reduced to zero. Therefore, the EU considers the CBAM as a key tool to address carbon leakage with a mechanism that seeks to ‘equalise’ GHG costs of imports with those of domestic production.

Last year, the European Commission (EC) invited the public to submit feedback on the legislative Roadmap on the CBAM, which is aimed at ensuring ‘that the price of imports reflects more accurately their carbon content’. The EC is also to design a new policy to reduce EU carbon emissions, addressing ‘carbon leakage’ and incentivising other countries to join emission reduction efforts.

The legislative Roadmap listed four options for the CBAM:

Until now, there has been no clarity on the design of the EC’s legislative proposal and on how the CBAM could work in practice. At the time of writing, a public consultation is being conducted, with submissions to be accepted up to Sept 10.

European Parliament’s stance

On March 10, 2021, the European Parliament adopted its position on the CBAM through a Resolution on ‘A WTO-compatible EU carbon border adjustment mechanism’. This position is to be taken into account by the EC, as it works towards the publication of its legislative proposal.

The Resolution underlines that the European Parliament supports the introduction of a CBAM ‘provided that it is compatible with WTO rules and EU free trade agreements by not being discriminatory or constituting a disguised restriction on international trade’; and that a CBAM ‘should be exclusively designed to advance climate objectives and not to be misused as a tool of protectionism, unjustifiable discrimination or restriction’.

Indeed, this should be the objective, but it remains to be seen if the EU will actually deliver on this or if the CBAM will protect EU businesses rather than the environment.

While the European Parliament assessed the four options being considered by the EC, the Resolution focuses on options 1 (import tax), 3 (which mirrors the ETS) and 4 (a ‘carbon tax’).

Most notably, the Resolution encourages the EC to pursue option 3 and to propose a CBAM based on the ETS. According to the European Parliament, while complying with WTO rules, the CBAM would need ‘to charge the carbon content of imports in a way that mirrors the carbon costs paid by EU producers’.

It should be noted that the option favoured by the European Parliament would not immediately affect the agricultural sector. In fact, under this option, the mechanism would mirror the ETS and its current coverage of sectors. The other options would not strictly follow the ETS sectors, which could mean that those options would cover a broader range of sectors, possibly including agriculture.

In its Resolution, the European Parliament recognised that products not falling under the ETS should be considered and that, in order to achieve the objectives of the European Green Deal, the CBAM mechanism should be accompanied by ‘necessary measures in non-ETS sectors’. Such measures could affect palm oil, as agriculture is a non-ETS sector.

The Resolution highlights that the option of an excise duty (option 4) on the carbon content of all consumed products – domestic and imported – would not ‘fully address the risk of carbon leakage’. It notes that this would be ‘technically challenging given the complexity of tracing carbon in global value chains and might place a significant burden on consumers’.

The Resolution further acknowledges that a fixed duty or tax on imports (option 1) could be a simple tool and would provide ‘a strong and stable environmental price signal for imported carbon’, but that – if the CBAM were to be of a fiscal nature – unanimity would be required in the Council of the EU.

Importantly, the Resolution ‘stresses that the CBAM should ensure that importers from third countries are not charged twice for the carbon content of their products’ and that ‘Least Developed Countries and Small Island Developing States should be given special treatment’.

Legal uncertainties

While the objectives of the CBAM are clear, many legal uncertainties remain. Consequently, the legal viability of the concept has yet to be determined. The EU should strive to develop a mechanism that complies with relevant WTO disciplines. How the EU designs and applies the CBAM will be crucial in determining its consistency with WTO rules, especially if the EU were to apply a border measure that only targets imports.

The General Agreement on Tariffs and Trade (GATT) prohibits WTO Members from imposing tariffs and charges in excess of the levels committed in their respective Schedule of Concessions. In addition, the GATT prohibits levying internal taxes or charges in excess of those applied to ‘like’ domestic products.

The European Parliament proposes a CBAM based on the ETS so as to ensure that both domestic producers and importers pay the same carbon price. Notably, a difficulty arises when assessing whether the charge levied by a WTO Member on an imported product is equivalent to that applied to the domestic product – for example, where the importing country does not maintain a simple tax scheme, but a more complex scheme, such as the ETS.

With respect to the issue of ‘likeness’ under Article III of the GATT on ‘National Treatment on Internal Taxation and Regulation’, processing methods cannot currently be used to classify two products as different (or not ‘like’). EU policies that discriminate against imported products vis-à-vis ‘like’ domestic products, based on how they are produced, risk being incompatible with WTO rules, notably with the non-discrimination principle. Therefore, a CBAM would run the risk of being inconsistent with WTO rules.

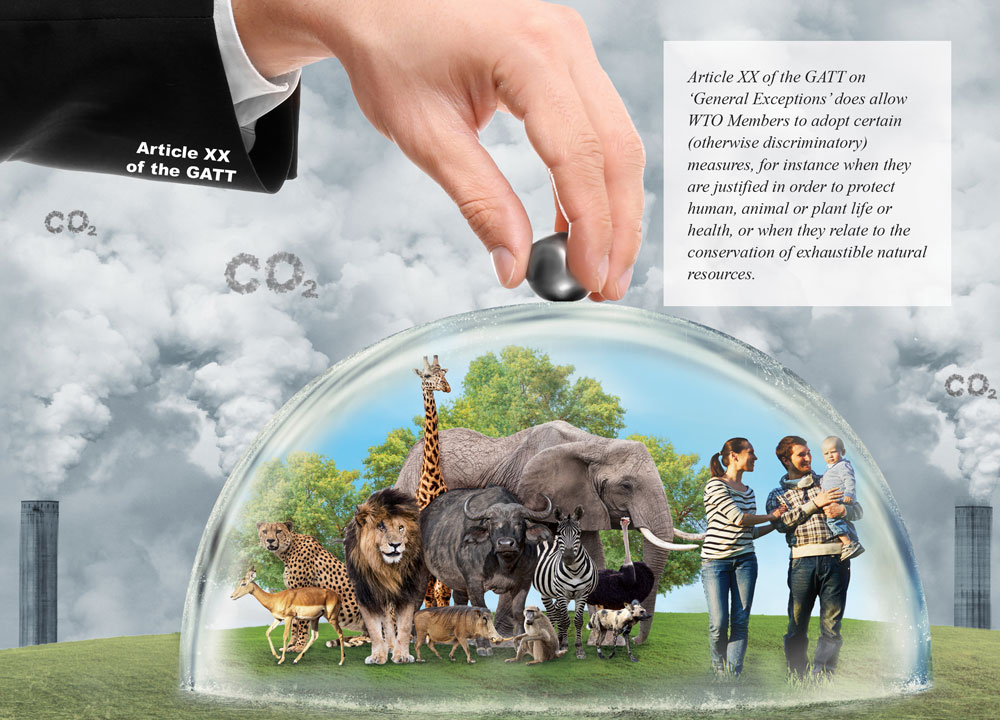

Article XX of the GATT on ‘General Exceptions’ does allow WTO Members to adopt certain (otherwise discriminatory) measures, for instance when they are justified in order to protect human, animal or plant life or health, or when they relate to the conservation of exhaustible natural resources. Both exceptions are subject to strict requirements and, over the years, in the majority of disputes, WTO Members have failed to successfully justify their environment-related measures under Article XX.

In particular, the exception for measures to protect human, animal or plant life or health would need to pass the necessity test; this would determine whether such measures are ‘necessary’ to achieve the policy objectives being pursued.

To consider a measure ‘necessary’, a WTO panel would need to assess the extent of the measure’s contribution to the achievement of its objective; and its trade restrictiveness in light of the importance of the interests or values at stake.

Concerns expressed

While the EU may be pursuing legitimate objectives with its environmental policies that drive up its costs, such regulatory requirements should not be detrimental to businesses around the world which are already subject to domestic requirements.

Countries like Australia, China, India, Indonesia, Japan and Singapore have already expressed concern, indicating that they perceive the CBAM as a unilaterally imposed and potentially protectionist measure that would be discriminatory and negatively affect trade.

They point out that countries in Asia and the Pacific region have been developing or already have their own carbon pricing approaches, which the EU might not be taking into account. Therefore, these countries have asked the EU to create a CBAM that would take their measures and mechanisms into consideration.

More specifically, certain Asian countries and in particular Indonesia and Malaysia, have called on the EU to work with third countries and not to take a unilateral decision that would cause a situation comparable to the discrimination of palm oil under the EU’s revised Renewable Energy Directive (RED II). Additionally, several countries have said that the EU should use the revenues generated by a CBAM to help developing countries in their decarbonisation efforts.

Any CBAM introduced by the EU must be implemented in the least trade-restrictive manner possible. However, it can already be expected that any such mechanism, regardless of its design, will be challenged by other WTO Members.

Given existing EU policies, such as the RED II, it should also be clearly advocated that the CBAM should not apply to agricultural products, including palm oil.

On April 26, 2021, EC Executive Vice-President and Commissioner for Trade Valdis Dombrovskis stated that the proposal on the CBAM was only the beginning of the discussion.

Stakeholders, including those in Malaysia, should therefore ensure that their perspectives and positions are heard, in order to achieve a balanced and non-discriminatory mechanism – ideally one that is based on multilateral approaches and not on unilateral obligations.

Dato’ Dr Wan Zawawi Wan Ismail

CEO, MPOC