2021 half-year report

September, 2021 in Issue 3 - 2021, Markets

Palm oil prices experienced a rally during the first half (H1) of the year, with the average monthly Malaysian delivered CPO price ranging between a high of RM4,572/tonne in May and a low of RM3,749/tonne in January. The Bursa Malaysia Derivatives Exchange’s CPO Futures (FCPO, Figure 1) third-month benchmark price also experienced a rally during this period, fluctuating between RM3,160 and RM4,525/tonne, trending lower after hitting a record high of RM4,525/tonne on May 12.

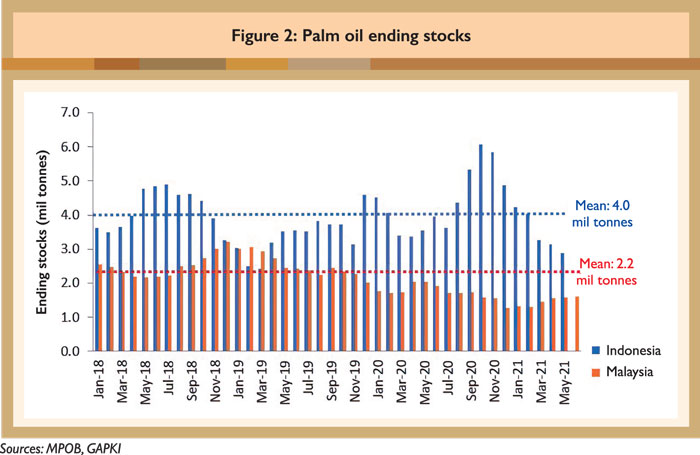

Low palm oil ending stocks in Indonesia and Malaysia kept prices firm. Indonesian Palm Oil Association data showed that Indonesia’s inventories were at 2.9 million tonnes for May, down 18% year-on-year. According to the Malaysian Palm Oil Board (MPOB), inventories in Malaysia were at 1.6 million tonnes for June, down 15% year-on-year (Figure 2). Supply disruptions and rebounding demand led by recovering economic activities from the second half (H2) of 2020 have kept inventories at below-average levels.

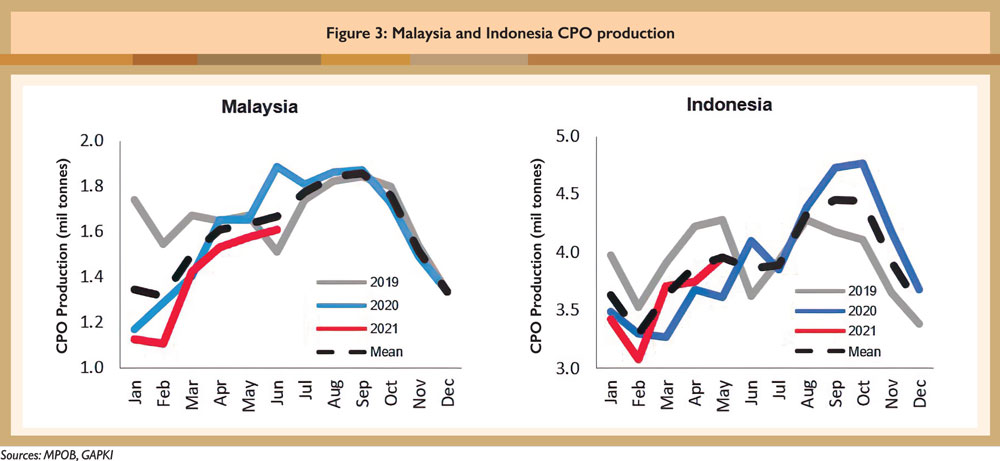

There has been a halt in palm oil output growth over the last three years (Figure 3), mainly due to wet weather conditions, remaining effects of prolonged drought in Q3 2019, lower fertiliser applications over the past few years and labour shortages (primarily in Malaysia). MPOB data showed that CPO production in Malaysia in H1 of 2021 totalled 8.4 million tonnes, down 7.6% compared to the same period in 2020. In contrast, Indonesian CPO production during the first five months of 2021 totalled 17.9 million tonnes, edging up by 3.2% year-on-year, indicating a faster production recovery.

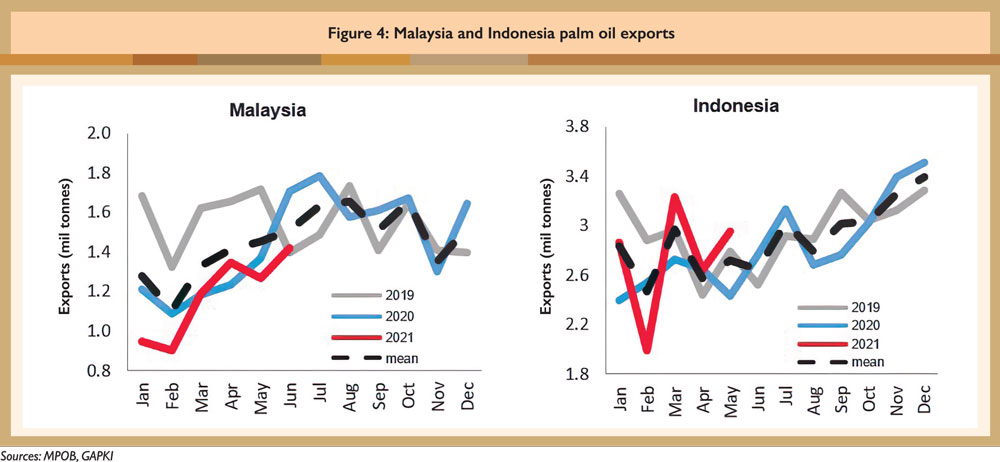

Year-to-date Malaysian palm oil exports were relatively subdued (Figure 4), totalling 7.1 million tonnes for H1, down 9.3% year-on-year. In contrast, Indonesian palm oil exports over the first five months of the year totalled 13.7 million tonnes, up 7.4% year-on-year.

Second half of the year

Production outlook

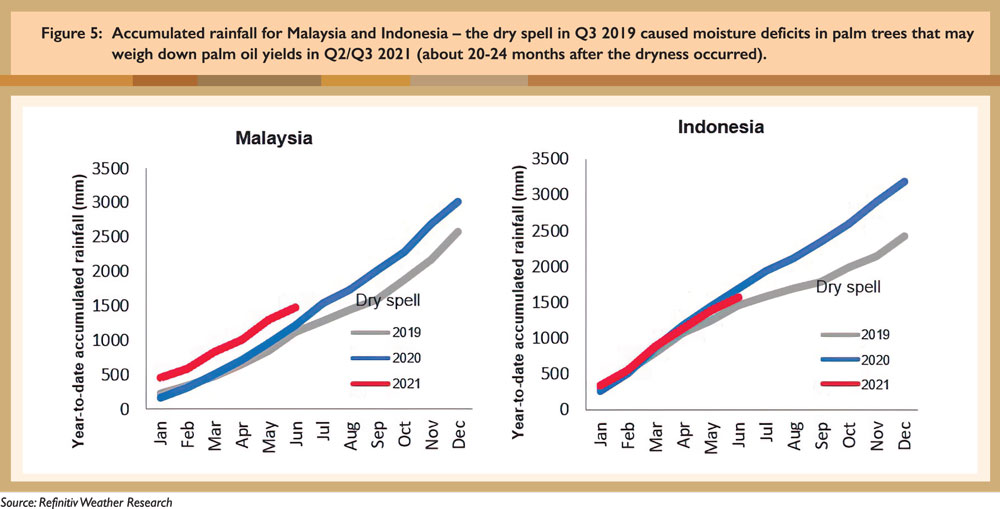

Indonesian CPO production for the whole of 2021 is projected to be higher by 1-3 million tonnes versus 2020 at 47-50 million tonnes. Malaysia’s production is expected to be around 18.7-19.3 million tonnes. The lagged impact of prolonged drought in Q3 2019 (Figure 5) and lower fertiliser applications over past years have capped the upside, but palm oil production in both countries will see seasonal recovery in H2 this year.

Indonesia is poised to have a more robust output recovery relative to Malaysia due to good estate management and no halt in operations or labour shortage. The Malaysian palm oil industry was short of approximately 31,000 harvesters, prompting significant crop losses. Progress in recruiting locals and bringing back foreign workers has been slow in the face of the Covid-19 situation.

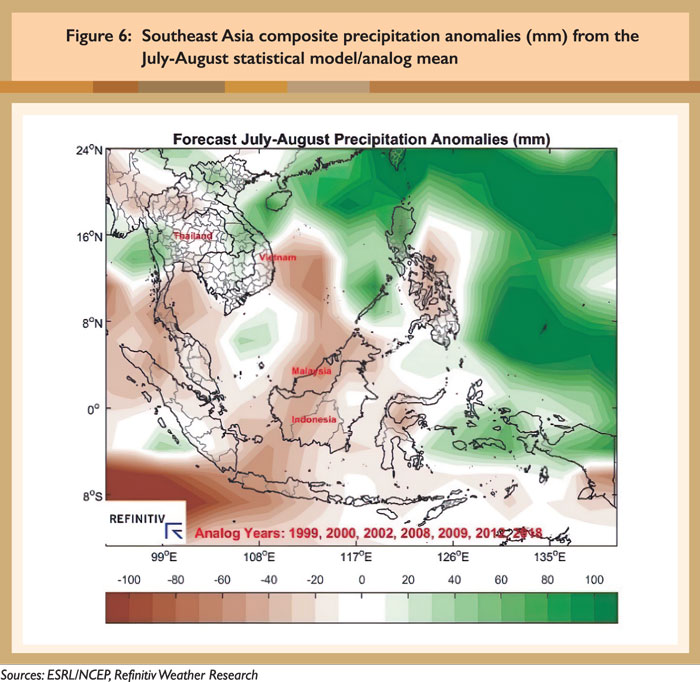

In terms of the weather outlook, the El Niño 3.4 region has trended warmer from a La Niña state towards a neutral negative ENSO state in recent weeks, which would bring drier-than-normal weather conditions across most palm-growing areas in Malaysia and Indonesia in July and August (Figure 6) if the trend continues. Lack of heavy rain will benefit harvest activities, boosting output during this period. September-November could feature wetter-than-normal conditions, which will largely favour oil palm growth in the region.

Demand outlook

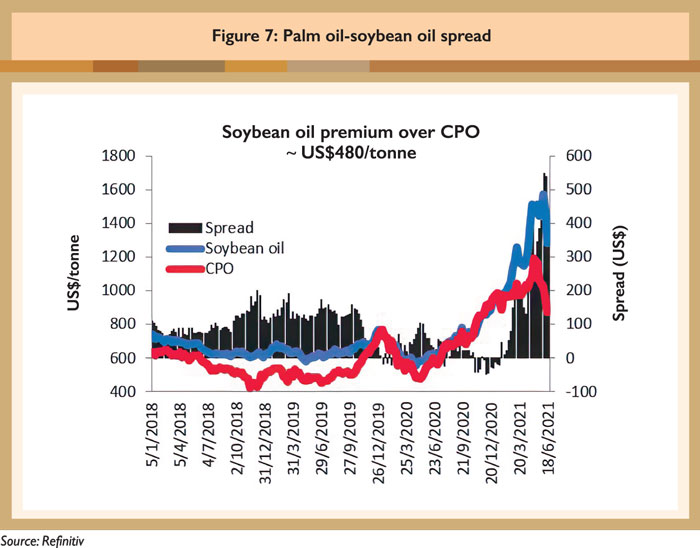

The demand outlook for H2 is pointing more towards upside, with the reopening of the hotels, restaurants and café sector amidst large-scale Covid-19 vaccination rollouts worldwide; this will boost demand in the food and non-food (e.g. oleochemicals and biofuels) industries. Demand is also underpinned by palm oil’s steep discounts to soybean oil, which widened to US$480/tonne by the end of June (Figure 7), making palm oil more attractive versus rival edible oils. The price correction in June has also attracted bargain buying.

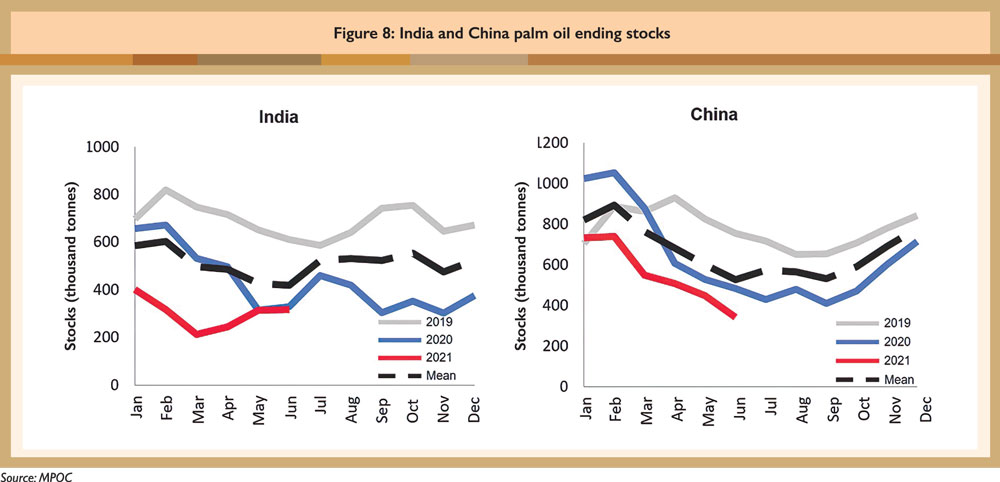

Palm oil inventories in India and China, the two largest consuming countries, remain low (Figure 8), encouraging replenishing activities. Stocks in China for June were estimated at 0.34 million tonnes, down 29% year-on-year, while inventories in India were at 0.32 million tonnes, down 4% year-on-year. Also, warmer weather in summer is conducive to blending, potentially boosting domestic consumption, further depleting inventories and encouraging demand.

Both key producing and consuming countries have revamped tariff structures in favour of boosting demand in H2.

Indonesia adjusted export levies for July, lowering the ceiling rate for CPO to US$175/tonne from US$255/tonne. The export levy starts when CPO prices hit US$750/tonne, with a US$20 increase for every US$50 rise in CPO. Palm oil export duties were also slashed to US$116/tonne for July, versus US$183/tonne in June, in response to falling CPO reference prices. The new palm oil levy is likely to lift exporters’ profit margin and prompt selling abroad.

Supported by the levies, the implementation of the B30 mandate in Indonesia remains an underpinning to sustain considerable domestic consumption since demand for the fuel has been evenly spread in 2021, according to a recent report by Indonesia’s state-owned oil company. The revision of export levies bears no impact on financial backing for the ongoing national replanting programmes targeting 180,000 ha in H2.

India, the world’s largest importer, lowered CPO import tariffs to 10% from 15% for three months, effective June 30, making the effective rate, including other tariffs, 30.25% versus the previous rate of 35.75%. Moreover, India removed RBD palm oil and RBD palm olein from the list of restricted items for a period of six months until Dec 31, prompting palm oil imports to become more appealing compared to rival edible oils. Buyers could take this opportunity to ramp up palm oil imports to meet high festive demand.

However, there are several downside risks for demand. Palm oil imports by key destinations, such as India, slumped earlier this year due to a resurgence of Covid-19 cases in the country. The continued impact of the pandemic will influence global consumption in the food and non-food sectors, and determine the pace of demand recovery in H2.

Also, bumper oilseed supplies in the months ahead and the EU’s policies will negatively impact the market. The revised Renewable Energy Directive (RED II) is poised to cap palm oil as a feedstock for biodiesel in the mid-to-long run. The Belgian government has notified the EU of a draft national decree that is poised to exclude palm-based biodiesel from its market from 2022. Moreover, the EU’s new food safety standards on 3-monochloropropane diol (3-MCPD) and glycidyl fatty acid esters (GE), contaminants found in refined palm oil products, are also expected to weigh on imports.

Price outlook

Palm oil prices have experienced a prolonged rally since last year, fueled by tight supplies and demand recovery. However, the rally tapered off in June (Figure 9). Worries about lacklustre demand and production recovery going forward have depressed palm oil prices recently. Erosions in external vegetable oil markets, such as the Chicago Board of Trade and the Chinese Dalian Commodity Exchange, have also weighed on sentiment.

As Malaysia and Indonesia have entered the peak palm oil production season, prices could be pressured by rising inventories. We believe that palm oil prices will stay elevated, supported by low inventory levels at both origins and destinations, but will remain volatile throughout H2, affected by other market drivers.

Bigger global oilseed production is on the way

Palm oil production is picking up and prices could face pressure if production increases significantly in the coming months. As Indonesia has a faster pace of recovery, H2 production will be dependent to a large extent on the weather factor and stability of estate management in supply performance. The current favourable levy structure is also expected to provide space for companies to increase production capacity, which will lend support to the enhancement of the downstream industry, R&D, scholarship and replanting programmes.

The pace of production recovery in Malaysia will depend on how soon the industry can get an adequate supply of foreign workers; as well as on yield recovery from 2019’s dryness and lower fertiliser applications from previous years.

The US Department of Agriculture (USDA) also indicates more oilseed supplies going forward, with the global soybean production for 2021/22 higher by 21.7 million tonnes from 2020/21 levels to 385 million tonnes. The USDA raised global soybean ending stock estimates for 2021/22 by 3 million tonnes from 2020/21 levels to 94.5 million tonnes, on the back of higher beginning stocks for the US and Brazil. Refinitiv Agriculture Research pegged global soybean production and ending stocks for 2021/22 at 385 million tonnes and 90 million tonnes respectively (estimates as at June).

The USDA raised global rapeseed production by 5.1 million tonnes to 74.1 million tonnes for 2021/22. Global sunflower seed production was raised by 7.3 million tonnes to 57 million tonnes in the coming season. A bumper sunflower crop from the Black Sea region will be entering the market to compete for a share in the months ahead.

Uncertainties in external policies

The US government policy on biofuels remains uncertain. Soybean oil prices tumbled after the news that the US government is considering providing oil refiners relief from the biofuel blending mandate, following a Supreme Court ruling to exempt small oil refiners from biofuel blending requirements. This will limit biofuel production, reducing demand for soybean oil. Talk that the Environmental Protection Agency is re-examining biofuel blending requirements adds to the uncertainty, with any unfavourable adjustments to biodiesel waivers likely to trigger another sell-off.

In addition, China’s plans to strengthen commodity price controls domestically, reflected by its move to auction imported corn and soybean oil to cool domestic prices, is also viewed as bearish for the market.

Supporting drivers

After a prolonged rally since last year, palm oil prices have been starting to moderate but will stay elevated. The historical peak of RM4,525/tonne in the five weeks from May 12 to June 18 – despite the recent bearish benchmark of FCPO of RM3,262/tonne – should keep the market optimistic. Year-to date average prices are de facto higher than an expected average of RM2,600-2,650/tonne.

The industry holds mixed views on the CPO price trend, with the Malaysian Palm Oil Council forecasting prices to range between RM3,500 and RM3,800/tonne in the coming three months, supported by rising export prospects while output is expected to increase marginally. Reuters technical analysis suggests that FCPO in Q3 may bounce to RM3,746-3,844/tonne, before dropping towards RM2,927-3,232/tonne levels. Some industry players also expect palm oil prices to soften further in H2 after registering an all-time high CPO price in May.

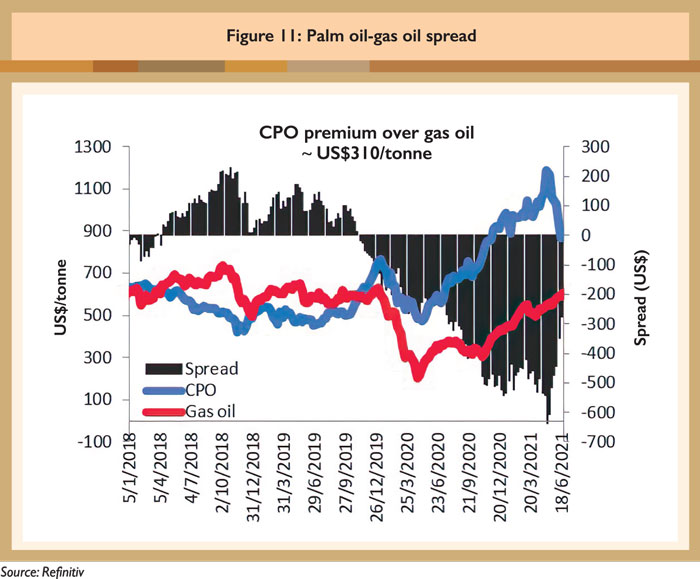

Price volatility will stay in H2. However, increased enabling environments in producer countries and encouraging demand especially from China and India, compounded by several supporting drivers in the near/mid-term should spark positive sentiment. Rising gas oil prices are supportive of the palm-based biodiesel market as Indonesia is progressing towards its output target of 9.2 million kilolitres, a target set for the B30 mandate this year.

Improved global demand will persist amidst mass vaccination rollouts, on the back of a steep discount to rival vegetable oils, low inventories in key consuming countries and favourable tariff structures. The US will be a factor to consider due to unfavourable weather, and biofuels policy that may lower the demand and output growth of soybean oil. This will give palm oil a likely advantage in H2.

Tan Kian Pang

Senior Analyst, Agriculture Research

&

Lim Suet Yiing

Senior Analyst, Oil Research,

Refinitiv

This is a slightly edited version of the report prepared by Refinitiv with feedback from the CPOPC Secretariat. The full version is available at: https://www.cpopc.org/wp-content/uploads/2021/07/2021_PALM-OIL-SUPPLY-AND-DEMAND-OUTLOOK-REPORT-WITH-REFINITIV-1.pdf