The second edition of MPOC’s Palm Oil Internet Seminar was held from Oct 18-24,2021. A panel of experts provided Oct 18-24, 2021. A panel of experts provided updated assesments on the global edible oils market, and reviewed the CPO price trend up to Q3 2021. They also shared insights into focus that may influence the price trend in Q4.

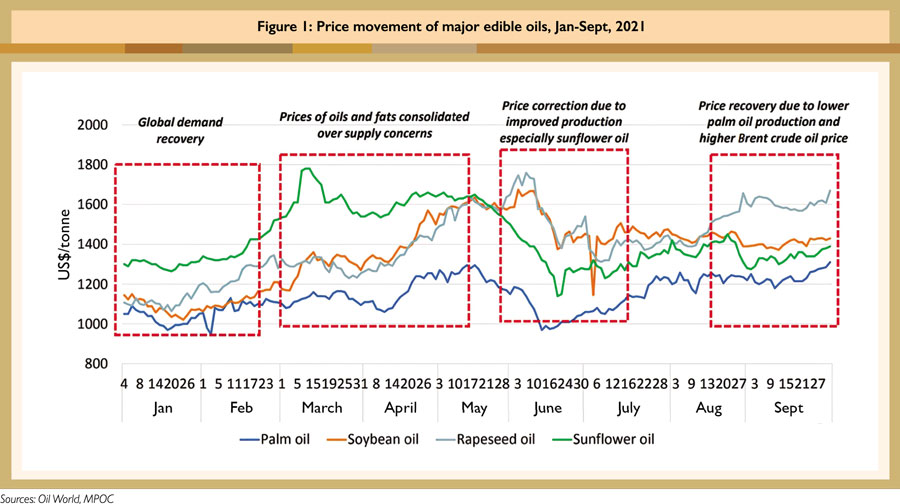

CPO prices rose sharply over Q1 and Q2 2021, spurred by the recovery of global edible oils demand. The palm oil industry benefitted from higher consumption, particularly by the hotel, restaurant and café sector worldwide; this had been drastically affected by the prolonged lockdown to curb the Covid-19 pandemic.

Strong demand was recorded from major palm oil importers like India, Iran, Turkey and Kenya, where stocks required replenishment. Demand also increased in Malaysia, due to celebration of the Muslim festival of Eid; a higher uptake of processed foods; and the soft reopening of industrial and business operations as the country emerged gradually from the lockdown.

In Q2, sentiments were affected by expectations of higher sunflower production in Ukraine and soybean output in the US. Another factor that contributed to price consolidation was speculation that Indonesia would cut its levy on CPO exports, which could lead to a larger outflow. Concerns over low stocks of CPO in Malaysia further influenced the trend of edible oil prices – in June, the stock level was below 1.7 million tonnes.

All four major oils had a consistently high value in Q3:

The price discount of soybean oil to palm oil in Q3 was US$250/tonne, an increase of US$81/tonne against the same period last year. The palm oil price sentiment was also affected by the seasonal peak production of oil palm from August to October.

Global edible oil prices began to recover in the final quarter of the year. The prospects of improved production of edible oils, especially sunflower oil, have been a significant driver. The price sentiment further turned positive on the news of lower Malaysian Palm Oil production, a weaker Ringgit and rising Brent crude oil prices.

Q4 2021 – Bullish factors

An array of bullish factors was observed to support the prospect of higher palm oil prices and bigger imports by major buyers.

China

Continued recovery from the Covid-19 pandemic and low inventories will drive imports of edible oils, including palm oil, in Q4 2021. Traders will likely import more palm olein due to lower domestic availability of soybean oil, as the poor breeding margin in the swine sector is expected to lower China’s soybean crushing activities. MPOC projects that China’s palm oil imports for the year will be 6.8 million tonnes, or 300,000 tonnes more than in 2020.

India

The country’s recent changes in import policy and duty cuts have contributed to the current price dynamics of palm oil. The removal of the ban on RBD palm olein imports from June to December 2021, and the reduction in import duty on all edible oils, are likely to push up India’s palm oil demand in Q4. The import duty reduction was aimed at bringing down edible oil prices which had risen by 14% in February and by 35% in June. MPOC estimates that India will import 8.7 million tonnes of palm oil for the year, compared to 1.2 million tonnes previously.

Malaysia

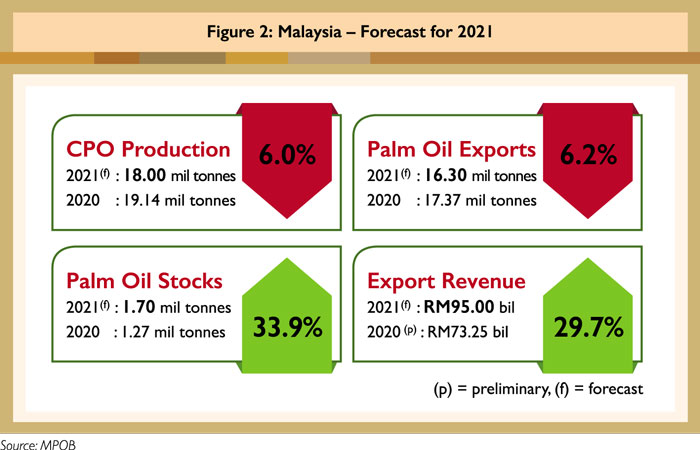

Palm oil production experienced a setback due to a severe shortage of labour. However, this is expected to have a positive impact on CPO prices. The production of Malaysian Palm Oil from January to September was recorded at 13.3 million tonnes, falling by 1.3 million tonnes (8.8%) against the same period last year.

MPOB expects Malaysian CPO production to decline to 18 million tonnes in 2021, or by 1.1 million tonnes (6%) year-on-year. As a result, MPOB forecasts that exports will drop by 6.2% over the comparative period. However, export revenue is anticipated to go up by 29.7% due to extremely high CPO prices particularly in the second half of 2021.

Q4 2021 – Bearish factors

The panel of experts also discussed factors which may have a bearish impact on price sentiments. Based on a forecast by Oil World’s Thomas Mielke, the US will have a bumper soybean crop in 2021, with production expected to rise by 6 million tonnes to 121 million tonnes. This may directly impact the CPO price rally recorded in October.

At the same time, it will be challenging for Indonesia – the world’s largest producer of palm-based biodiesel – to achieve its targeted output of about 7 million tonnes, if the FAME and Gasoil spread goes higher than INR5,000 per litre as at October.

Another bearish factor is a decline in palm oil imports by EU member-states. Several European governments have opted for early adoption of the revised Renewable Energy Directive (RED II), which will phase out palm oil use in biofuels by 2030. Austria, France, Belgium and Germany have adopted RED II ahead of implementation due from 2023. For 2021, MPOC forecasts that the EU will import about 7.8 million tonnes of palm oil, or about 400,000 tonnes less than the 2020 imports of 8.2 million tonnes.

CPO price sentiments in Q4 2021 may be affected by higher global output of oils and fats. For the 2021/22 season, Mielke predicts that global production will increase by 8 million tonnes – the biggest volume in the last four years. With this sizeable increase, edible oil stocks too will rise and subsequently weaken the CPO price.

The bearish factors may have an impact on CPO prices in the first quarter of 2022. However, several members of the expert panel predicted that the average CPO price will remain high until the end of 2021. MPOC projects CPO to trade within a range of RM3,517- 4,745/tonne, achieving an average of RM4,131/tonne for the year. MPOB puts its estimate at an average price of RM4,100/tonne.

As for the CPO price outlook for Q4 2021, Oil World is of the view that the current high prices of palm oil and other vegetable oils are not sustainable. However, should the South American soybean production prospects deteriorate significantly, the CPO prices have potential to remain high in the current price range. The weakening of the CPO price will be moderated by lower production in Malaysia.

Lim Teck Chaii

MPOC

Details of the presentation and discussion can be viewed at: www.pointers.org.my