Post-pandemic outlook remains bright

December, 2021 in Issue 4 – 2021, Markets

The Covid-19 outbreak has had a devastating impact on the global economy over the past two years. Governments have been feverishly attempting to adapt to the rapidly changing dynamics and mitigating the impact of the pandemic. The lockdowns and movement restrictions caused 114 million people to lose their jobs in 2020, while food prices continued to rise.

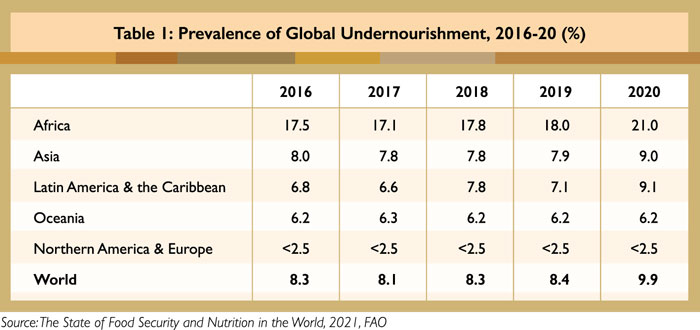

The unpredictability and volatility brought on by Covid-19 have intensified discussions related to nutrition and food security. People in low- and middle-income countries generally feel the impact more severely (Table 1), because they spend a larger share of their earnings on food than those in high-income countries. Fortunately for the food sector, palm oil has been produced without interruption to meet global nutrition and food security needs in terms of edible oil.

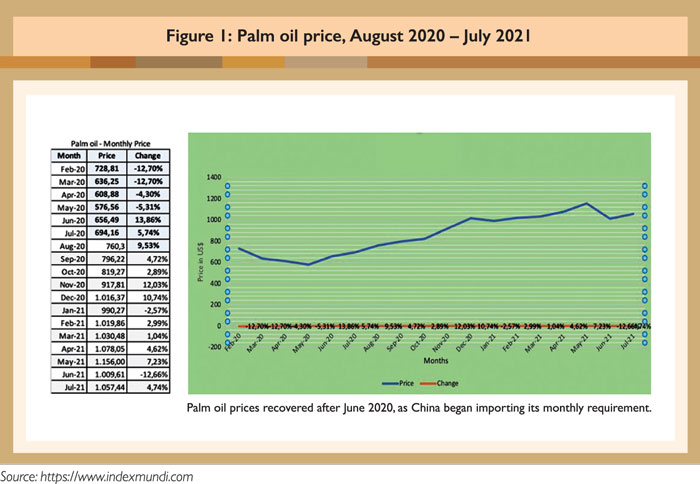

As the pandemic began to be realised in February/March 2020 and lockdowns were imposed – first, in China and later in other countries – palm oil prices began to fall. It was speculated that, with the lockdowns, demand for palm oil by the hotels, restaurants and café (HORECA) sector would be reduced and prices would be further weakened. Producer countries projected reduced imports by buyers.

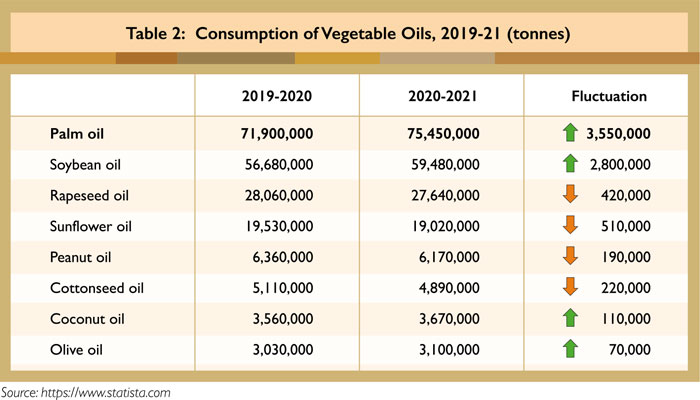

However, the palm oil industry in Indonesia and Malaysia was allowed to continue operating during the lockdowns. As a result, production continued to increase in 2020 and 2021 in Indonesia. Malaysian production was affected by labour shortage, as workers could not be hired back by the plantation companies due to travel restrictions. But overall, palm oil was sufficiently and sustainably produced to provide added food security for the world (Table 2).

The initial fall in the price of palm oil was attributed to China’s inability to import the commodity, as the lockdowns disrupted logistics in the supply chain. China had to use its existing stocks while waiting to import palm oil again. The price recovered after June 2020, as China began importing its monthly requirement (Figure 1).

Since then, palm oil prices have remained relatively high compared to historical levels, reflecting strong demand. This has some interesting implications as it may indicate new challenges and opportunities for the oil palm industry going forward.

On hindsight, continued palm oil production was a good thing for the consuming countries in terms of enhancing their food security. For the producer countries, the much-needed revenue supported weakened economies. Demand for palm oil remained robust, as low consumption in the HORECA sector was offset by increased use in home cooking and takeaway food services, arising from ‘stay at home’ and ‘work from home’ policies to curb the spread of Covid-19.

Market-related aspects

The long-term, post-pandemic outlook for the palm oil industry remains bright. Since the last quarter of 2019, palm oil supply and demand are back in balance, while stocks are declining. Prices have been relatively high for most of 2020 and 2021.

The increased revenue has been very welcome to producer countries. Oil palm farmers have received good prices for fresh fruit bunches. Also, they have not been as badly affected as workers in other sectors who have been subjected to lockdowns, pay cuts and job losses.

Consumers, however, have been affected by the high prices of oil and fats. The lower supply of rapeseed and sunflower oil, as well as strong demand for soybean and its oil, have led to the recent high price of soybean oil. But the lower price of palm oil relative to soybean oil has benefitted consumers, especially those whose incomes have been affected by the economic slowdown due to the pandemic.

The current trend of a long period of high prices experienced by palm oil – and other oils and fats – may be part of a new long-term shift in the supply and demand balance of these commodities.

While demand for oils and fats has grown due to the expanding global population, palm oil supply may not be growing at as high a rate as in the past. The moratorium on new land expansion for oil palm cultivation in Indonesia and similar lack of new land in Malaysia have limited the growth rate of palm oil production in recent years and in the long term.

As other oils and fats have been growing at a lower rate than palm oil, it is unlikely that the next major crop – such as soybean – will grow at a super-high rate to compensate for the lack of rapid expansion in palm oil production. Therefore, the future supply of oils and fats has to experience a slowing growth relative to demand. Prices have to rise to reflect this new supply and demand balance. If this outlook holds true, palm oil producers will see good returns.

Maximising the production of palm oil will have to be pursued by improving yield through better agronomic practices. If the industry can seize the opportunity to improve the yield by 50% – as with other oilseed crops – more than 35 million tonnes of palm oil can be additionally produced per year, without any land area expansion. This represents an opportunity for a huge increase in revenue for producers, given the projected high prices in the near future.

Proven benefits of palm oil

Palm oil plays a crucial role in providing the world with food oil as a source of consumers’ oils and fats requirement. Better affordability and availability compared to other oils imply that palm oil offers consumers the opportunity for assured food security. The main challenge is to enhance awareness of the nutritional properties of palm oil for better acceptance.

Numerous studies have suggested that palm oil provides beneficial health effects as a dietary oil. The proven evidence is embodied in a clinical study in the US on the cholesterol ratio effect of palm oil when blended with soybean oil or rapeseed oil as part of the diet. Consuming palm oil in such blended form helps improve the good HDL to the bad LDL ratio. The blended palm oil products have been commercially marketed in the US with success, and carry a FDA-approved label which says ‘patented blend to help improve cholesterol ratio’.

It is also known that, depending on the type of refining, palm oil is the richest source of beta-carotene, a natural source of pro-Vitamin A, and a great source of tocotrienols or Vitamin E. For refined red palm oil, the pro-Vitamin A carotene content is up to 15 times more than in carrots. Opportunities to supply consumers with a nutritionally beneficial blend based on red palm oil containing high levels of pro-Vitamin A beta-carotene and a potent level of antioxidant tocopherols and tocotrienols can only be offered by palm oil.

An estimated 80% of palm oil is used for food consumption. The CPOPC fully supports the importance of food security, adopting the global view that ‘no food means no human beings’. With high population growth, static agricultural land growth, and long-term effects of the pandemic, how will we secure the basic need of nutritious food for the world’s 10 billion human beings by 2050?

Addressing this challenge will require efficient and sustainable agri-food systems that are able to produce safe and adequate nutrients for everyone. No one should be left behind in accessing the fundamental right to food and to be free from hunger.

Opportunity to achieve UN goals

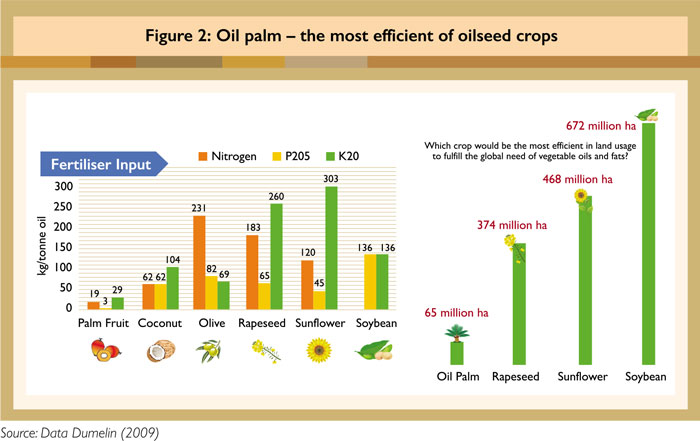

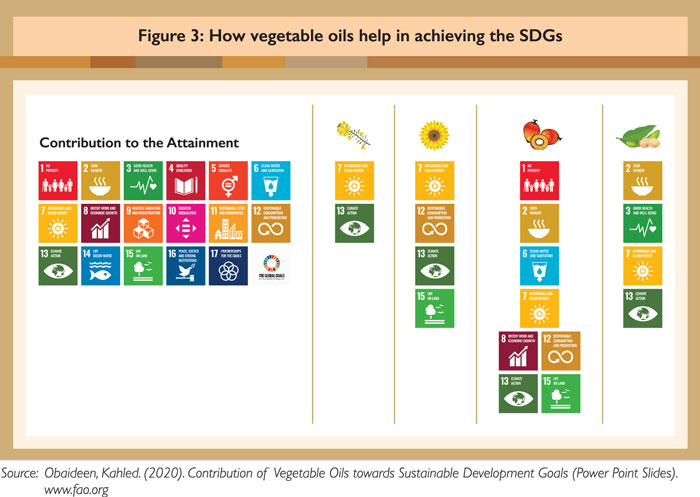

The oil palm is simple to grow because it is more efficient, uses less land, and needs less pesticides and fertilisers than other oilseed crops (Figure 2).

Palm oil is the best crop for cultivation in producer countries as it can be their vehicle to attain most of the UN Sustainable Development Goals (SDGs) by 2030 (Figure 3). Palm oil can help achieve13 of the 17 SDGs. As 40% of palm oil production is by smallholders, attaining the SDGs will also directly improve their economic and social welfare.

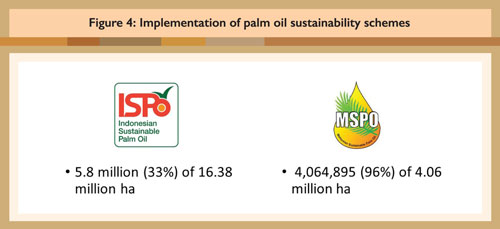

The attainment of the SDGs poses the challenge that palm oil production must itself be done sustainably. In this regard, producer countries are way ahead in organising the certified sustainable production of palm oil, compared to the non-existent or minimal capability for certified sustainable production of competing oils. Malaysia and Indonesia have each imposed mandatory certification of palm oil production, via the Malaysian Sustainable Palm Oil (MSPO) and Indonesian Sustainable Palm Oil (ISPO) standard respectively.

At the time of writing, Malaysia had achieved 96% certified sustainable palm oil (CSPO) production (Figure 4). This is reinforced by other certification schemes, giving buyers the option to choose what they prefer. In Indonesia, almost 6 million ha of plantations have been certified, including most of the large and state-owned plantations managed by companies.

Goal No. 12 of the SDGs highlights the need for sustainable production and consumption of food or edible oils and fats. CSPO supplies will deliver such benefits. In addition, trade in palm oil adds to economic growth, employment, food security and other SDG objectives in consuming countries. Thus, both producing and consuming countries can share the benefits.

Beating smear campaigns

There are not many challenges facing the palm oil industry which cannot be mitigated over time. The pandemic may have started the new trend of high prices for oils and fats. In the long term, the high prices may be attributed to supply growth limitations, resulting from the lack of new land for oil palm cultivation as a result of persistent anti-palm oil campaigns by NGOs.

It follows, though, that the actions of NGOs to discourage the expansion of oil palm cultivation have affected consumers, who pay higher prices for oils and fats. Palm oil producers are not much affected as they are well compensated when the price is high.

Similarly, European Union (EU) campaigns to ban the use of palm oil in its biofuel programme will have the unintended effect of causing greater environmental damage – the vegetable oils that will replace palm oil in biofuels will require much more land for their production. Palm oil producer countries, meanwhile, have built their biodiesel production and consumption capacity so that palm oil usage remains strong.

The situation has exposed the EU protectionist policy in trade, and palm oil producing countries are right in seeking to correct such unfair trade practices through complaints to the WTO. However, environmental lobbyists and some NGOs are expected to continue pressuring governments and corporate boards of palm oil consuming countries, particularly in the EU, to issue policies and initiatives that are counter-productive to opportunities offered by palm oil.

They continue to try to discredit palm oil by standing on the argument that it should be removed from the food supply chain (via the ‘no palm oil’ label) and substituted with other crops, using the unfounded allegation that oil palm cultivation causes deforestation. This dangerous and unrealistic scenario should be discontinued because the alternative crops are actually far behind oil palm on social, economic and environmental metrics.

Since the CPOPC was established in 2015, it has persisted in countering smear campaigns against palm oil. The CPOPC is and will be working closely with its current and future member-countries to maintain a sustainable supply chain in industry. Collective efforts will be strengthened with consuming countries to eliminate the trade-off between competing policy objectives and beating the smear campaigns against palm oil.

Palm oil is truly part of the solution and not part of the problem. Why? Because having this renewable resource guarantees that the world will always have a sustainable option to not run out of oil for nutrients, food and other purposes, not only for today but also future generations.

Tan Sri Datuk Dr Yusof Basiron

Executive Director, CPOPC,

Jakarta, Indonesia

This is an abridged version of the keynote address, ‘Overview of the World Palm Oil Industry Moving Forward: Challenges and Opportunities’, presented at the 2nd Edition of the World Palm Virtual Exhibition & Conference, on Sept 7, 2021. The full speech is available at: https://www.youtube.com/watch?v=oR–1iS15j4&t=15s