Sub-Saharan Africa, with more than 40 countries and a population exceeding 1 billion, has become a substantial market for palm oil over the last 10 years. However, domestic palm oil production has been insufficient to meet the region’s needs.

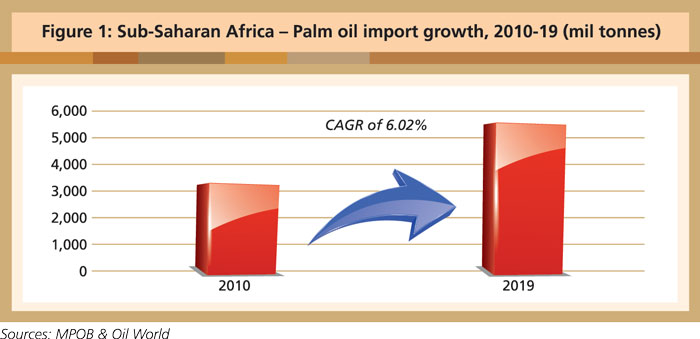

In 2019, African countries produced about 2.8 million tonnes of palm oil, but demand stood at about 7.3 million tonnes. Imports therefore play an important role, already having recorded a compound annual growth rate of about 6% between 2010 and 2019 (Figure 1).

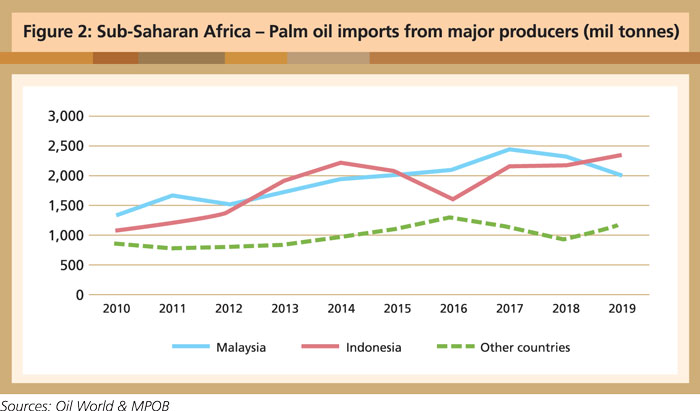

The use of Malaysian palm oil has kept pace with the region’s import volume. From 1.3 million tonnes in 2010, Malaysia’s contribution went up to a record high of 2.4 million tonnes in 2017. However, it then dipped slightly to 2.3 million tonnes in 2018 and to about 2 million tonnes in 2019 (Figure 2), due mainly to competition in a price-sensitive market.

West African countries provided about 2.8 million tonnes of palm oil in 2019. Nigeria was the biggest producer with 1.2 million tonnes. The Ivory Coast was the only net exporter, with 510,000 tonnes of production and 282,000 tonnes of exports. Ghana and Cameroon are other suppliers from the region.

The bulk of the palm oil imported from Malaysia and Indonesia by countries like Benin and Togo is rerouted to adjacent west African countries due to the favourable tax structure. Similarly, imports by Kenya and Mozambique are sent on to neighbouring landlocked countries in east and southern Africa.

The region’s refining industry has expanded rapidly over the last 10 years in tandem with changes in consumer choices and better economic conditions. Nigeria, Ghana, Kenya and Mozambique all have a large refining capacity now. In 2011, CPO/CPL constituted merely 3.8% of palm oil products imported from Malaysia. In recent years, CPO/CPL imports have grown to more than 40% of the total volume.

Tanzania, once a major importer of CPO, switched to RBD palm olein after the government increased the import duty on CPO from 10% to 25%, in response to pressure from domestic oilseeds producers. Countries like Benin, Togo, Angola and South Africa also prefer RBD palm olein. The region’s demand for specially-packed cooking oil fell from a high of 483,000 tonnes in 2011 to just 107,000 tonnes in 2019.

Bolstering trade

The Malaysian palm oil industry has much to gain by enhancing policy and business strategies, in order to make further inroads into Sub-Saharan Africa. The region’s palm oil market is growing rapidly, driven by rising consumption of processed food and fast food, among other changes. Viewing its countries as places of opportunity for collaboration would bring about mutual benefit. Two main strategies hold out possibilities.

Through the years, free trade agreements (FTA) have grown in importance and scope worldwide. These do not just reduce and eliminate tariffs, they also help address barriers that would otherwise impede the flow of goods and services. In addition, they encourage investment and facilitate market access.

However, Malaysia has yet to sign a FTA with any African country and, therefore, faces impediments by way of tariff barriers. To change this, Malaysia would not have to negotiate for lower tariffs with each country. It could negotiate with a bloc such as the African Continental Free Trade Area. This would streamline the process and unlock business opportunities more quickly than through negotiations with individual countries.

Despite Malaysia’s long presence in Africa, many in the oils and fats business are relatively unaware of investment opportunities, because of lack of information. In 2011, with investments of US$19 billion. Malaysia was Africa’s most important Asian investor, ahead of China and India in terms of the size of its foreign direct investment.

Currently, though, Malaysia lags behind investors from Indonesia and Singapore. Malaysian palm oil traders need to consider setting up joint ventures and partnerships to improve their market share.

They could also consider investing in storage, bulking and manufacturing facilities in the region to facilitate the production and distribution of Malaysian palm oil. The restaurant and café sectors are other segments that could yield high returns from the use of palm oil. Such ventures would help accelerate the local economy through new jobs and higher purchasing power, and boost demand for Malaysian palm oil.

Iskahar Nordin,

Marketing Executive,

Marketing & Market Development, MPOC