Industry update

October, 2018 in Issue 3 - 2018, Markets

The Malaysian oil palm industry had put in a sterling performance in 2017. Crude palm oil (CPO) production and fresh fruit bunch (FFB) yield were significantly better, following recovery from the impact of the El Nino phenomenon a year earlier. According to the Department of Statistics Malaysia, higher palm oil prices and improved demand helped push export earnings to RM77.85 billion, up from RM67.92 billion in 2016.

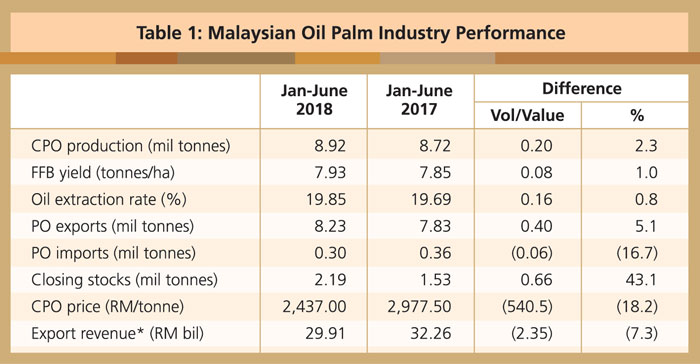

The first half of 2018, however, showed a mixed performance against the same period in 2017 (Table 1). CPO production and export demand grew, but imports declined. Higher carry-over stocks, coupled with vigorous production, pushed palm oil stocks above 2 million tonnes in the first half of 2018. Weaker vegetable oils prices took a toll on the CPO price, thereby affecting export revenue.

Source: MPOB, *Department of Statistics Malaysia

CPO production in the first half of 2018 went up by 2.3% to reach 8.92 million tonnes, compared to 8.72 million tonnes in the first half of 2017. The larger output was attributed to the amount of FFB processed, arising from improved FFB yield. The yield rose by 1% to 7.93 tonnes per ha, from 7.85 tonnes per ha during the corresponding period in 2017. The oil extraction rate (OER) increased by 0.8% to 19.85%.

Palm oil exports rose by 5.1% to 8.23 million tonnes, against 7.83 million tonnes in the first half of 2017. But prices were lower, thereby reducing export earnings from oil palm products including palm oil. Due to its lower price, palm oil imports declined by 16.7% to 0.3 million tonnes, from 0.36 million tonnes previously.

Supply and demand scenario

Opening stocks

2018 started with 63.9% higher carry-over stocks of palm oil, which stood at 2.73 million tonnes compared to 1.67 million tonnes in 2017. This was due to increased CPO production in 2017 – up by 15% or 2.6 million tonnes to 19.92 million tonnes, against 17.32 million tonnes in 2016.

CPO production

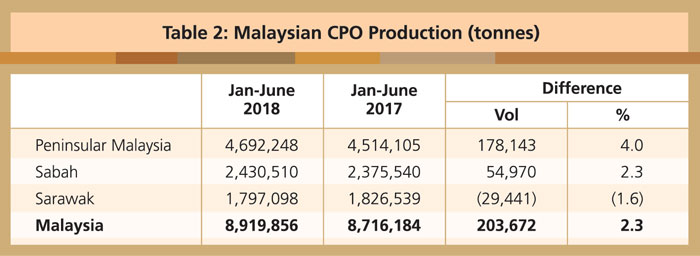

CPO production in the first half of 2018 registered 8.92 million tonnes, up by 2.3% or 0.2 million tonnes against 8.72 million tonnes in the first half of 2017 (Table 2). Higher FFB yield enabled mills to process more FFB, leading to additional CPO output. Production in Peninsular Malaysia and Sabah recorded an increase of 4% and 2.3% respectively, to 4.69 million tonnes and 2.43 million tonnes. Production in Sarawak showed a slight decline of 1.6%, to 1.8 million tonnes.

Source: MPOB

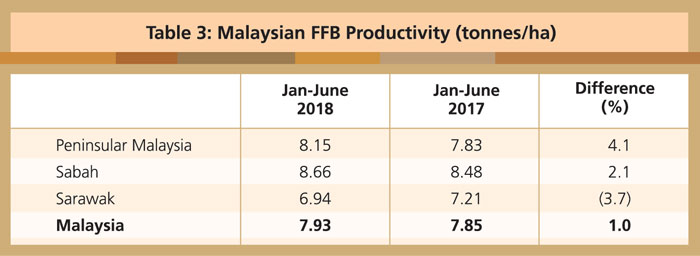

Malaysia’s FFB yield performance in the first half of 2018 was 7.93 tonnes per ha, or 1% more than the 7.85 tonnes per ha achieved during the comparative period in 2017 (Table 3). The increase in FFB yield was partly attributed to conducive weather conditions.

Source: MPOB

Peninsular Malaysia and Sabah showed an increase of 4.1% and 2.1% respectively in FFB yield to 8.15 tonnes per ha and 8.66 tonnes per ha in the first half 2018. Sarawak registered a decline of 3.7% to 6.94 tonnes per ha in the first half of 2018 from 7.21 tonnes per ha previously. This was associated with additional mature areas coming into production.

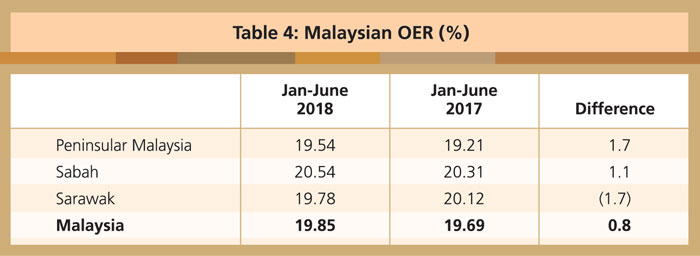

The average national OER for the first half of 2018 was 19.85%, slightly higher by 0.8% against 19.69% during the same period of 2017 (Table 4). This was mainly due to the better quality of FFB processed by mills. On a regional basis, the OER in Peninsular Malaysia and Sabah increased by 1.7% and 1.1% respectively to 19.54% and 20.54%. Sarawak showed a marginal decline at 19.78%, or 1.7% lower than 20.12% in the first half of 2017.

Source: MPOB

Exports

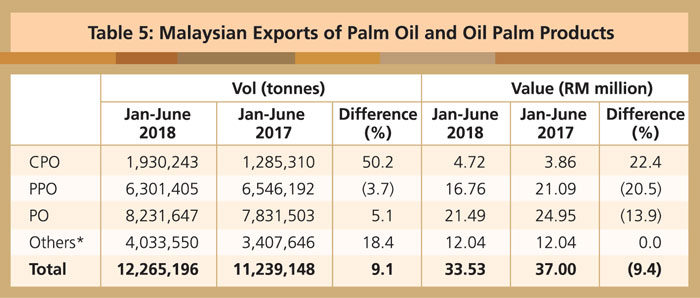

Exports of oil palm products for the first half of 2018 amounted to 12.27 million tonnes, higher by 9.1% against 11.24 million tonnes during the same period in 2017 (Table 5). However, due to the lower prices in the world market, the total export value declined by 9.4% to RM33.53 billion, against RM37 billion during the first half of 2017.

*PKO, PKC, oleochemicals, biodiesel, finished products & others

Source: MPOB

Palm oil exports increased by 5.1% to 8.23 million tonnes, against 7.83 million tonnes for the period under comparison. Higher demand was registered from major importing countries such as India, Pakistan, China and the EU. The palm oil export value, however, declined by 13.9% to RM21.49 billion, from RM24.95 billion during the first half of 2017.

The decline in export revenue during the first half of 2018 was due to the fact that all oil palm products traded at lower prices compared to the same period in 2017. CPO traded lower by 17.8% or RM524/tonne to record RM2,420.50/tonne, compared to RM2,944.50/tonne during the first half of 2017. The lower price was partly due to India raising its palm oil import duties and weaker soybean oil prices in the world market. In addition, the stronger Ringgit versus the US Dollar made palm oil comparatively more expensive for holders of foreign currencies.

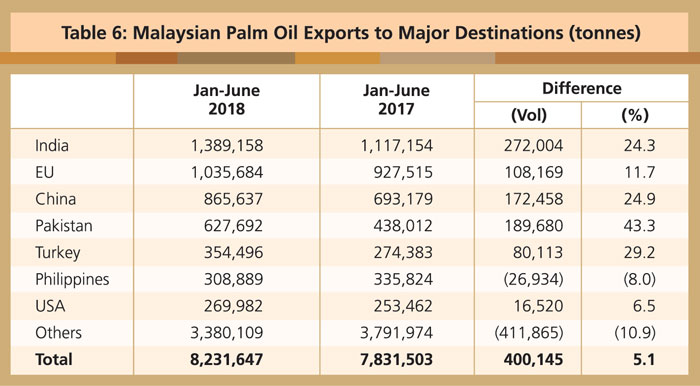

For the first half of 2018, India maintained its position as the largest Malaysian palm oil market with an intake of 1.39 million tonnes or 16.9% of the volume exported (Table 6). The EU was ranked second with 1.04 million tonnes or 12.6% of the palm oil exports. China (10.5%), Pakistan (7.6%), Turkey (4.3%), the Philippines (3.8%) and USA (3.3%) were other important destinations. These seven markets together accounted for 4.85 million tonnes or 58.9% of Malaysian palm oil exports during the first half of 2018.

Source: MPOB

With respect to market destinations, palm oil exports to India increased by 24.3% to 1.39 million tonnes during the first half of 2018, up from 1.12 million tonnes during the corresponding period of 2017. The increase was partly attributed to the suspension of Malaysia’s CPO export duty from Jan 8 to April 30, 2018. India also lowered its intake of soybean oil from Argentina – it went down by 33.4% to 860,000 tonnes from January-May 2018, from 1.2 million tonnes during the same period in 2017.

Exports of palm oil to the EU increased by 11.7% to 1.04 million tonnes vis-à-vis 0.93 million tonnes during the first half of 2017. This was due to lower intake of sunflower oil by 26.2% to 0.73 million tonnes, compared to 0.99 million tonnes during the same period in 2017.

China’s imports of Malaysian palm oil saw a significant increase of 24.9% to 0.87 million tonnes from 0.69 million tonnes previously, due to lower soybean imports from Argentina and Brazil. The soybean import volume fell by 8.9% to 35.74 million tonnes from January-May 2018, compared to 39.25 million tonnes from January-May 2017.

During the first half of 2018, Pakistan recorded a 43.3% increase in Malaysian palm oil imports, which stood at 0.63 million tonnes against 0.44 million tonnes in the same period of 2017. This was a result of lower imports of Indonesian palm oil – which dropped by 14.7% to 0.66 million tonnes – and lower intake of soybean from Brazil (by 23.2% to 0.51 million tonnes) for crushing activity.

Palm oil intake by Turkey expanded by 29.2% to 354,496 tonnes, compared to 0.27 million tonnes from January-June 2017. This was attributed to lower imports of sunflower oil from January-April 2018, especially from Russia.

Imports

Malaysia’s imports of palm oil over the first half of 2018 stood at 0.3 million tonnes, a decline of 18.3% from 0.36 million tonnes during the same period in 2017. The ample local supply satisfied lower demand from the domestic processing sector, especially refineries, given that there was smaller export demand for processed palm oil. This was partly attributed to the suspension of duty on Malaysia’s CPO exports. Indonesia remained the major source of palm oil imports, contributing 94.9% or 0.28 million tonnes.

Palm kernel oil imports declined by 27.4% to 77,645 tonnes during the first half of 2018. The local oleochemicals sector registered lower demand for the commodity on the back of lower export demand for oleochemicals – this fell by 0.8% for the period under comparison. Imports of palm kernel increased 2.5-fold to 33,312 tonnes. There was higher demand from the crushing industry, driven by a 24.9% increase in export demand for palm kernel cake.

Closing stocks

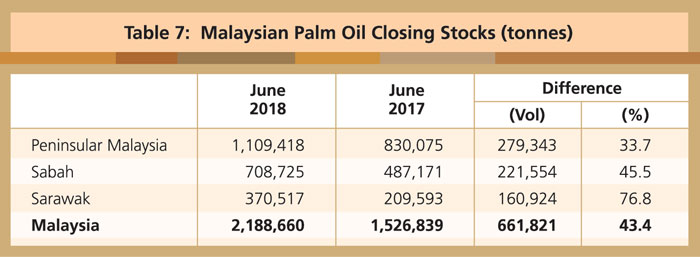

Palm oil closing stocks as at end June 2018 increased by 43.4% or 0.66 million tonnes to 2.19 million tonnes. In comparison, 1.53 million tonnes were recorded in June 2017. The situation was mainly due to the higher opening stocks (up by 63.9% or 1.07 million tonnes) and larger output from January-June 2018, which was 2.3% or 0.2 million tonnes more than in the same period in 2017 (Table 7). All regions in Malaysia recorded higher closing stocks in June 2018 against June 2017:

• Peninsular Malaysia – higher by 33.7% to close at 1.11 million tonnes

• Sabah – an increase of 45.5% to 0.71 million tonnes

• Sarawak – 76.8% more to 0.37 million tonnes

Source: MPOB

Outlook for second-half 2018

The rise in CPO production in the first half of 2018 is expected to continue into the second half due to anticipated good weather. CPO production in 2018 should keep to its normal upward trend that starts in March and peaks in September. It will decline from October to December, under the normal downward trend.

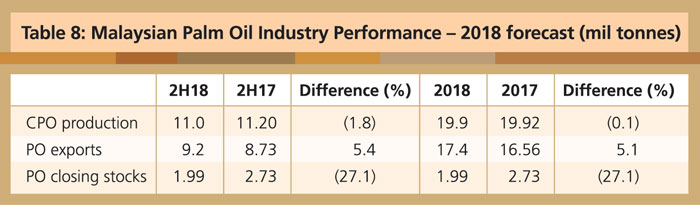

In the second half of 2018, CPO production is projected at 11 million tonnes, reflecting a marginal decline of 1.8%. The corresponding period in 2017 had recorded 11.2 million tonnes because of lower FFB yield, due to lower rainfall (Table 8). For the whole of 2018, CPO production is forecast at 19.9 million tonnes or a decline of 0.1%, compared to 19.92 million tonnes in 2017.

Source: MPOB

The palm oil export performance during the second half of 2018 is expected to improve over the first half. Low prices are expected to remain a major factor in supporting the increase in exports in the second half of 2018. The export volume is estimated at 9.2 million tonnes, an increase of 5.4% compared to 8.73 million tonnes during the same period in 2017. Total palm oil exports in 2018 are expected to go up by 5.1% to 17.4 million tonnes against 16.56 million tonnes in 2017.

Based on the anticipated higher exports in the second half of 2018 and likely lower production, closing stocks of palm oil in December 2018 are projected at 1.99 million tonnes, lower by 27.1% compared to 2.73 million tonnes in December 2017 (Table 8).

A Kushairi, Director-General &

N Balu, Director, Economics &

Industry Development Division,

Malaysian Palm Oil Board