Promising prospects for palm-based products

July, 2020 in Issue 2 - 2020, Markets

The agro-based economy of Bangladesh accounted for 20% of the GDP in 2019. Cattle and poultry farming contributed about 1.5%. About 70% of the population of 169 million live in rural areas. They deem livestock farming to be an asset in food production, both to raise incomes and women’s employment, and to alleviate poverty.

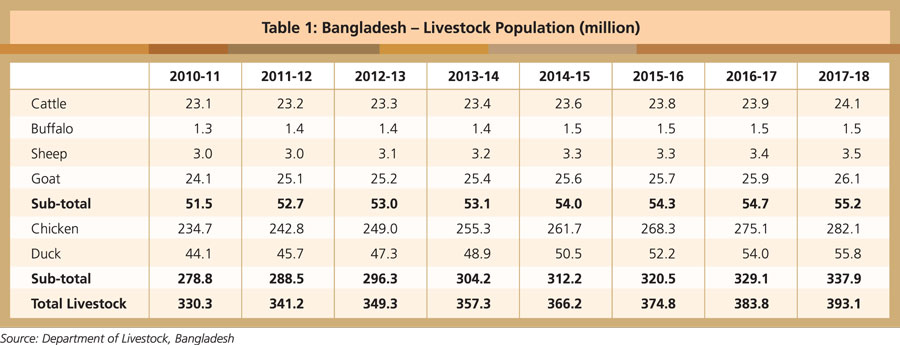

Due to increased demand, poultry, cattle and fish farms have gained prominence over the last two decades (Table 1). Alongside this, low-cost commercial feed production has experienced substantial growth over the last 10 years. This has, in turn, influenced demand for ready-mix feed, forcing the exit of smaller, low-quality producers with lower economies of scale. More than two-thirds of the market is dedicated to poultry feed. The cattle feed market remains the most under-developed of the three sectors.

Most dairy farmers mix home-made and commercial feed as a means of optimising costs. This is one area where Malaysian palm kernel expeller (PKE) and PKC/meal could perform well because of their competitive price.

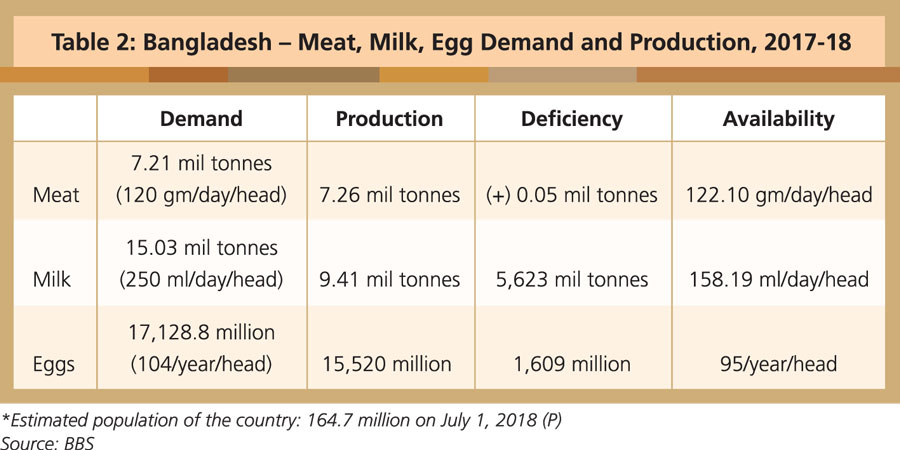

Annual demand growth for milk is estimated at 9-10%. Based on per capita meat and milk consumption, there is a latent demand of 50%. The Food and Agriculture Organisation puts per capita annual meat consumption in Bangladesh at 4.4kg against the recommended 10kg by World Health Organisation standards, while milk consumption is 158 ml against the recommended 250 ml per head per year (Table 2). As such, there are tremendous growth opportunities for the cattle farming and feed sectors.

Feed meal sector

Naturally grown grass has been a traditional component of fodder for cattle. Diversification to produce quality feed and fodder, as well as strengthening of the feed milling capacity and pasturage systems, would help to raise the productivity of livestock.

Bangladesh produces about 15,000-20,000 tonnes of molasses. It further makes about three million tonnes of soybean meal from domestic sources and imports, as well as oil cake from local oilseeds. Additional sources of feed come from 100,000-120,000 tonnes of paddy straw, fruit and vegetable waste annually. All these go into pre-mixed feed production, but this is still inadequate to meet demand.

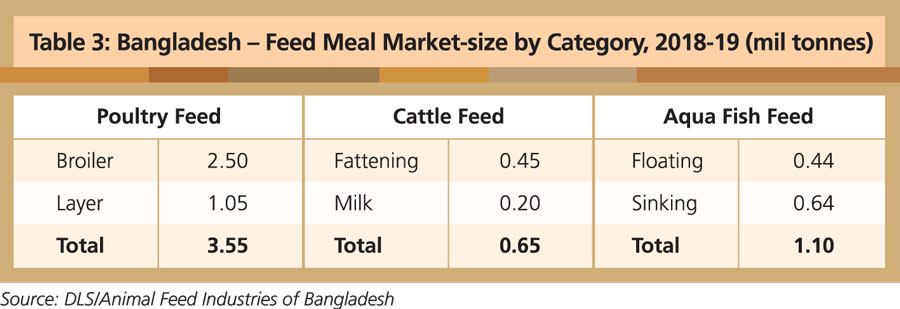

The Bangladesh chapter of the World Poultry Science Association estimates that the current feed meal market-size is about 5.3 million tonnes, with annual growth of about 8-9%. Bangladesh’s commercial feed industry can be divided into three categories, each with two sub-categories (Table 3). Broiler poultry feed currently holds the strongest position, with an average market share of 47.2%. Aqua fish feed is next (20.8%), followed by layer poultry feed (19.8%) and cattle feed (12.3%).

Although it makes up the largest segment, the broiler feed market is projected to grow the least. Fattening cattle feed, currently the smallest sub-segment, is expected to grow the fastest at a rate of about 15.5% annually, with milk cattle feed at a rate of 11.5%. Higher demand is being generated by Bangladesh’s steady economic growth of 7% in recent years, population growth, rapid urbanisation and change in dietary habits.

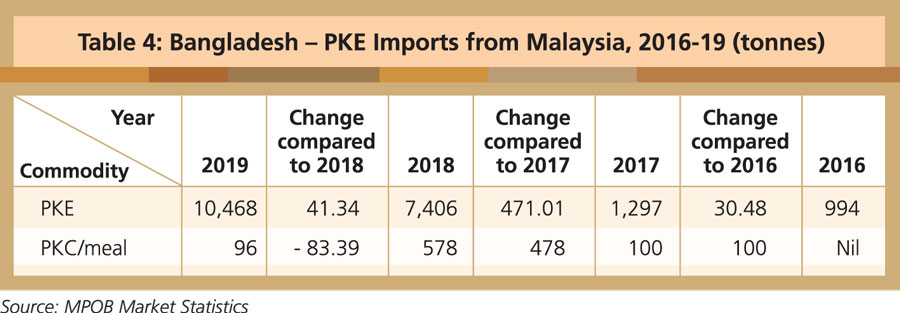

In line with the expansion of cattle farming, PKE imports have been growing quickly for the feed market. Imported PKE was introduced to Bangladesh a few years ago. Its price competitiveness and nutritional value are the main factors behind the demand growth (Table 4).

Malaysia is the only supplier of PKE and PKC/meal in Bangladesh at present. By educating cattle farmers, feed producers and formulation experts on the nutritional advantages and price competitiveness of PKE and PKC/meal, it could well command the market.

MPOC Bangladesh