Uncertain market for palm oil

February, 2017 in Issue 1 - 2017, Markets

Another remarkable thing about the UK market is that it imports similar quantities of palm oil and palm kernel meal, with the latter being mainly for the production of animal feed. According to a report by the UK Association of Animal Feed Producers, 11 million tonnes of feed were produced in 2014 – equivalent to 8% of the EU total and 1.2% of global output.

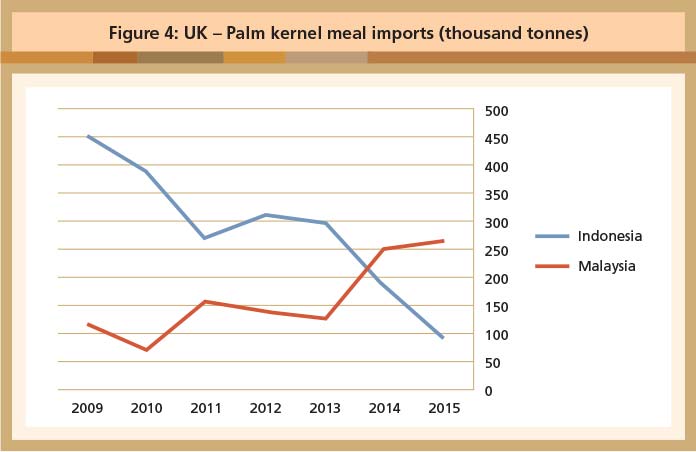

Malaysia, and Indonesia supply 93.2% of the palm kernel meal (Figure 4). In 2014, Malaysia became the leading exporter of the product to the UK, and maintained the lead in 2015.

Question marks now surround the future of the UK palm oil market. There may be some fallout from possible political instability. After the Brexit vote on June 23, 2016, the value of the Pound Sterling fell to a 30-year low. A weak currency would make imports more expensive, and demand may slump.

Sustainability issues may also come into play. For instance, a report by the green NGO Transport & Environment has claimed that 45% of all palm oil used in Europe in 2014 was in the form of biodiesel (edie.net, June 1, 2016). This represented a six-fold increase since 2010, and was swiftly dubbed ‘Biodieselgate’.

Reacting to the report, the UK Renewable Energy Association said that ‘UK import and consumption of palm oil-based biodiesel has fallen dramatically, and stands at zero so far in 2015/16’.

Brexit – if followed by a recession – may present an opportunity for the palm oil industry because buyers will start looking for competitively-priced options. However, zero consumption of palm oil for biodiesel would turn out to be a hard blow indeed.

MPOC Brussels

Pages : 1 2