Five reasons for optimism

February, 2017 in Biofuels, Issue 1 - 2017

However, the soybean oil market seemingly overreacted given the nuances of the biofuels market. Back in May 2016, the EPA proposed the advanced category be set at 4 billion gallons, which would be split between biodiesel and cellulosic biofuels with important implications for Renewable Identification Numbers (RINs).

Biodiesel RINs are based on an ethanol gallon equivalency of 1.5-1.7, depending on the type of biodiesel. Thus, one wet gallon of biodiesel generates 1.5 or 1.7 RINs. The weighted average for the overall supply of biodiesel is about 1.54 RINs/wet gallon.

Accordingly, the 2 billion gallon volume established for the biodiesel category will actually generate about 3.08 billion ethanol-equivalent RINs. Adding to the biodiesel RINs is the cellulosic category of 311 million RINs. As a result, the proposed volumes provided for a residual volume for undifferentiated advanced biofuel of 609 million gallons.

In setting the final volume for advanced biofuel at 4.28 billion gallons, however, 280 million gallons were added to the overall advanced biofuel category, making the undifferentiated category grow to 889 million gallons. There is unlikely to be a supply of either cellulosic or other qualifying undifferentiated biofuel to fulfil this category, meaning most of it will be made up by excess biodiesel. Indeed, if biodiesel were to make up all of this category, it would require about 577 million wet gallons of physical biodiesel, implying a mandate of 2.577 million gallons.

Trends through September in biomass-based diesel and renewable diesel production in the US plus imports indicate the total biodiesel supply is likely to reach nearly 2.5 billion gallons. This would suggest the market overreacted to the EPA announcement, and yet the January soybean oil contract closed the month at $0.37.

The biggest threat to the biodiesel sector is the fate of the $1 per gallon blenders’ tax credit, which was set to expire on Dec 31, 2016. Congress did not extend the Bill during the lame-duck session, and any further action on the credit will have to wait until 2017.

There is a slight chance a tax reform package may move through Congress in 2017 that could apply the credit retroactively. Moreover, it is possible that potential legislation could reform it into a producers’ credit instead, but the odds are very high that there will be no credit to start 2017. The safer bet is that Congress will take up tax reform in 2018.

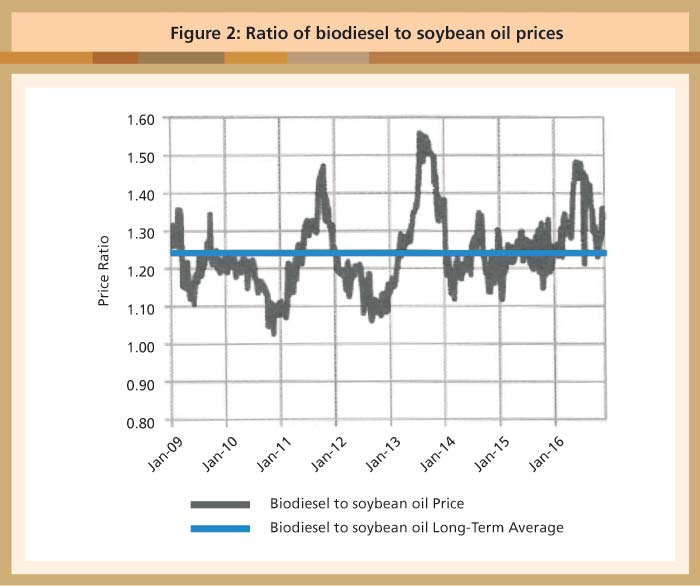

The tax credit has faced expiration before. According to a paper by Scott Irwin of the University of Illinois that analysed a representative Iowa biodiesel plant, ‘The Profitability of Biodiesel Production in 2016: Feasting on an Expiring Tax Credit?’ (farmdocdaily. illinois.edu, July 27, 2016), the biodiesel industry was profitable in 2011 and 2013, which were both years when the credit faced expiration. During those years, blenders bid up the price of biodiesel to secure the value of the credit, making biodiesel production profitable.

An analysis of the ratio of biodiesel prices to soybean oil prices (Figure 2) shows that 2016 is following the same pattern as 2011 and 2013, whereby the yearly ratio is exceeding the long-term average. Based on the price action of 2012 and 2014 (years following credit expiration), biodiesel profitability is likely to fall again in 2017.

Source: USDA, WPI